We contrarians profit on analyst dislike.

Note that I did not say like. Dislike is where the dividend money is at!

Analyst ratings are a wonderful buy signal. Vanilla investors purchase payers that are widely liked—and wonder why every downgrade dents their pocketbook.

We don’t care about popularity. Heck, we prefer stocks that are far from being in analyst good graces.

Give us the disgraces. And we’ll collect our dividends while we sit back and wait for the analyst upgrades to follow.

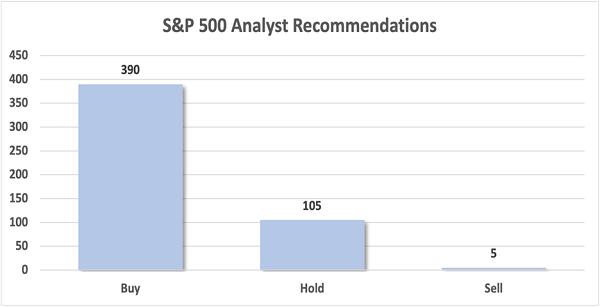

It’s not easy to find the “uncool kids” on Wall Street. The school of S&P 500 is a joke. Everyone gets an award (a Buy rating):

Source: S&P Global Market Intelligence

Four in five stocks are buys. What a market!

Let’s consider the discarded one in five, my fellow contrarian. Today I have handpicked eight loathed dividend payers dishing between 5.9% and 18.3% annually. Hated for a reason? Perhaps—or perhaps not.

Moelis & Co. (MC)

We start with independent global investment bank Moelis & Co. (MC, 5.9% yield), which provides numerous advisory services, most notably in mergers and acquisitions (M&A).

Moelis has nary a buy to its name following a 2022 that saw M&A activity fall off a cliff. The situation hasn’t improved much in 2023—the banking crisis has further muddied the M&A waters—and Moelis is just a month or so removed from another earnings miss. In the short-term, things could get even worse for MC than they already are. But keep your eye on Moelis longer-term, as robust hiring in its tech arm could represent the underpinnings of future growth.

Xerox (XRX)

One of the biggest names in printing continues to fight for relevancy.

Xerox (XRX, 6.6% yield) sells printers and digital document services in more than 160 countries nationwide. The latter business makes sense in the modern office—the former, less so. Xerox already was facing reduced paperwork heading into the COVID office exodus. And while employers are pushing for a return to the workplace, it’s clear that hybrid situations are here to stay—meaning overall less demand for Xerox’s core products.

XRX is also friendless in the analyst crowd, with zero buys at present. That’s despite a yield of nearly 7% and an extremely cheap valuation: its price/earnings-to-growth (PEG) ratio is a lowly 0.6. But I think the pros are right here—Xerox might be cheap, but it’s not a value.

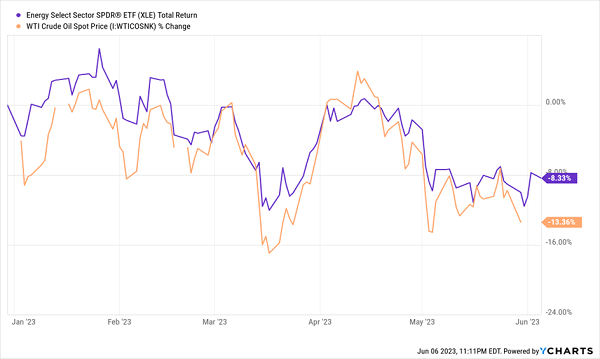

Energy Stocks

Crude’s slowdown in 2023 has taken energy stocks with it, saddling the sector with a loss despite an up year for the broader market.

Texas-based CVR Energy (CVI, 7.5% yield) deals in renewable fuels and petroleum refining, as well as nitrogen fertilizer manufacturing through its interest in CVR Partners LP (UAN). It hacked its payout in half during COVID—not abnormal for the space. However, while CVI did begin to restore it this year, there’s not much room for celebration. Last year’s massive special dividends seem unlikely to repeat unless oil goes bananas again, based on comments from CVR Energy’s Q1 conference call. But more importantly from that same call: A spinoff of their UAN stake could warrant a review of their regular dividend. Analysts’ bearishness seems deserved here.

Holly Energy Partners LP (HEP, 7.8% yield) has a single buy call, but that lone wolf might have the right idea. HEP, formed in 2004 by HollyFrontier—now HF Sinclair (DINO)—provides petroleum product and crude oil transportation, terminalling, storage and throughput storage. The company’s recent results have been boosted by HollyFrontier’s acquisition of Sinclair, as well as higher revenues on its Woods Cross refinery processing units. This newfound tailwind should widen its dividend coverage—raising the prospects of a distribution raise, which would begin a long climb back from a near-halving of the payout in 2020.

Cheniere Energy Partners LP (CQP, 9.4% yield) is another unpopular master limited partnership (MLP), boasting just two buy calls against six holds and six sells. It was created by Cheniere Energy (LNG) to hold its midstream assets; it owns Louisiana’s Sabine Pass liquefied natural gas (LNG) terminal, as well as the Creole Trail Pipeline.

CQP has been a perpetual quarterly distribution raiser for years—small steps each quarter, but steps that have added up over time. That said, the MLP came up against a brick wall this year, as it actually announced a ~4% decrease in May. Regardless, the company’s full-year guidance of $4.00-$4.25 per unit would be an improvement over 2022. My concern: CQP is starting an expensive Sabine Pass expansion—one that could draw resources away from the distribution as early as next year.

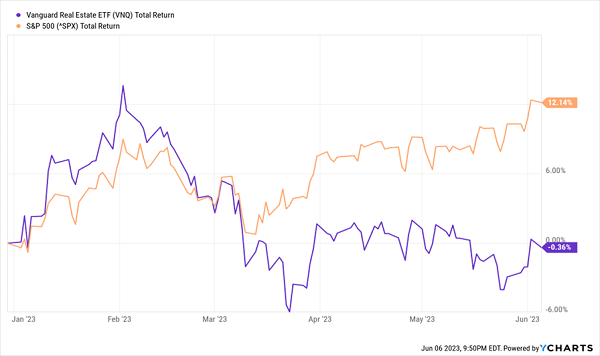

REITs

Wall Street is generally disenchanted with real estate investment trusts (REITs) right now, and for good reason. Jerome Powell’s lead foot has kept the interest-rate pedal down, rattling the sector loose. Real estate has underperformed since the start of the bear market, and is still flat in 2023 against a 12% gain for stocks more broadly.

A Rough Time for REITs

In short: There are plenty of hated stocks in the space. But are there any you can trust?

LTC Properties (LTC, 6.8% yield) invests in a 50/50 blend of senior housing and skilled nursing properties from coast to coast. While the worst of COVID has long passed, the operating environment remains difficult for LTC. After the end of Q1, LTC allowed one tenant to defer interest payments, another to defer monthly rent, and a third will receive an abatement. Long-term, there’s no denying the importance and stickiness of these kinds of properties, but there’s little in the way of short-term catalysts.

An even more troubled area of real estate is office property. Take Office Properties Income Trust (OPI, 12.2% yield), for instance. It owns nearly 160 primarily single-tenant office properties across the U.S. Shares are off nearly two-thirds over the past year and now trade in the single digits. Work-from-home would seem to doom the likes of OPI, though the REIT is an outlier operationally: Most of its properties are suburb-based, not city-based, and its occupancy rate is north of 96%. Still, I’ve largely agreed with the bearish analyst camp—I’ve recommended avoiding OPI in the past, and readers who heeded that advice dodged a 55% dividend cut announced in April.

Most analysts are on the fence concerning Hudson Pacific Properties (HPP, 18.3% yield). HPP leases out office and studio properties up and down the West Coast, from L.A. all the way up to Vancouver. Hudson’s office issues mirror the rest, but in March, I also flagged the potential hit from Hollywood’s writers strike. Well, in May, the company withdrew its full-year FFO outlook thanks to uncertainty from the strike—and more importantly, waved a white flag for its dividend. “The Company’s Board of Directors approved a 40% to 50% reduction in the common stock dividend, with the exact amount to be determined later this month.” That exact amount hasn’t yet been announced, but even halving the dividend would leave behind a yield in the high single digits, and a much healthier payout ratio of roughly half of first-quarter adjusted funds from operations (AFFO).

How to Retire on Just $500K

But let’s be serious. Just how “safe” would that 8% or 9% on Hudson Pacific shares actually feel? HPP is doing what it has to do, but such a sizable cut shows just how fragile the REIT’s positioning really is.

Buying HPP for that fat yield is a gamble—a roll of the dice.

It’s not a retirement plan.

A real retirement plan is building a portfolio that can generate at least 8% in reliable dividends. And that 8% is an important number—one that could allow you to retire on dividends alone, even with a smaller nest egg of, say, $500,000 to work with.

The math is easy: At 8%, you’re generating $40,000 in cash from your retirement account alone. Combine that with Social Security, you’ll have plenty to work with once you’ve moved on from your career.

And if you have an even bigger pile of cash to plug into our 8% “No Withdrawal” Retirement Portfolio, you’re looking at a downright cozy retirement—one where you’ll never have to touch your original nest egg!

The low-volatility stocks above don’t quite fit the bill. But I have plenty of stealth payout plays that do yield the 8% or more that we need to coast forever on dividends alone. Please click here and I’ll share the details on these secure funds with very generous dividends!