The 10-year Treasury rate has sunk to around 4%. And we’re going to cash in.

No, we’re not purchasing Uncle Sam’s sorry paper. Instead we’re picking up a basket of ridiculously cheap bonds paying more than 2X the beaten-down payout on the 10-year.

And the lower Sam’s rate falls, the more we profit, since bond prices rise as the 10-year yield, pacesetter for rates on loans of all types, drops. Our play here is through closed-end funds (CEFs) like the two we’ll discuss below, yielding up to 10.3%.

Why Treasury Yields Are On the Mat

There are lots of reasons floating around in the media about why Treasuries are falling, a “slowing” economy chief among them.

Could have fooled me!

As I write this, the Atlanta Fed’s GDPNow indicator—the most up-to-date measure we have—is pointing to 3.9% growth in the just-finished third quarter. Red hot! Consumer spending is holding up just fine, too, up 0.6% in August.

So why are Treasury rates falling? And why do I see them heading lower? For that, we need to look away from Wall Street—and toward DC.

Trump and Bessent Take the Heat Out of Rates

Truth is, we saw this lower yield coming months ago, when Treasury Secretary Scott Bessent straight-out said he’s focused on the “long” end of the yield curve.

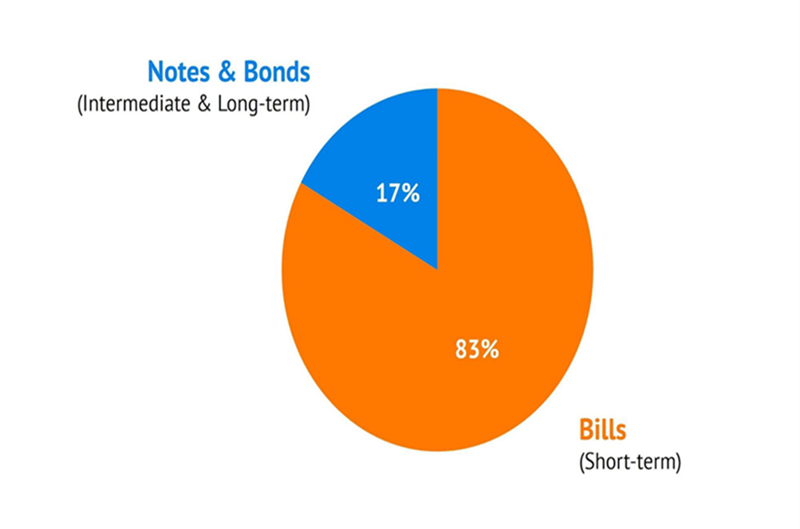

He’s gone after the 10-year rate, as we pointed out in our October 14 article, by shifting toward short-term issues—whose rates are set by the Fed—to fund Uncle Sam’s massive debt.

It’s a practice Janet Yellen started and Bessent once criticized—but then not only continued but amped up when he took over. Nowadays, he’s funding 83% of debt issuance short term.

The takeaway is that these moves lower supply of long-term Treasuries, boosting their prices and cutting their yields. Bessent then uses the cash raised by these short-term issuances to buy more longer-dated notes.

It’s a recycling program for Uncle Sam’s debt! And it leaves even fewer long-dated Treasuries for investors to buy.

Result? The 10-year rate has dropped from a high of 4.8% near the start of the year to around 4% now.

Bessent’s “Yield Cap” in Full Effect

Remember too that midterms are coming, so we can expect Bessent to keep up the pressure on Treasury yields (and the mortgage rates that are tied to them—the administration will do anything to lower those!).

That puts a solid floor, plus some upside, under corporate bonds. Which is where those two CEFs come in.

PIMCO Knows Bessent’s Playbook—and It’s Set to Pay Us 10.3% a Year

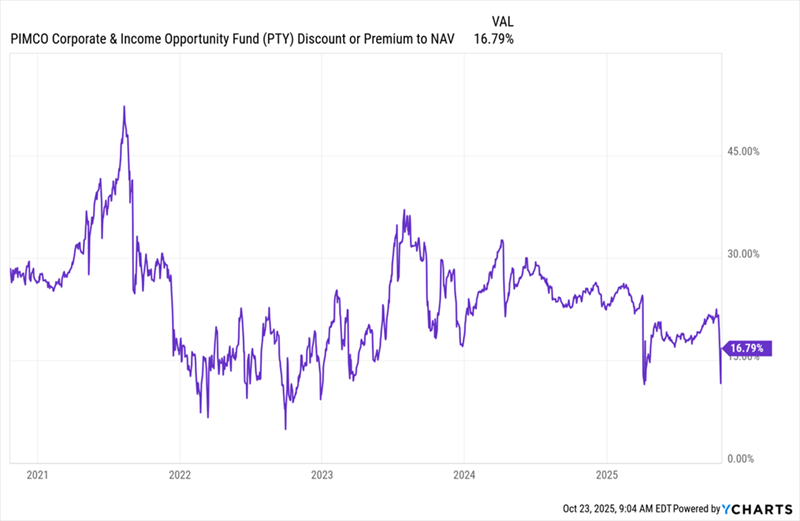

The PIMCO Corporate & Income Opportunity Fund (PTY) might not seem like a bargain at first, at a 16.8% premium to NAV. That means investors are paying $1.17 for every dollar of PTY’s assets.

But with CEF discounts, context is everything. Because PTY is actually on sale—though you won’t see that unless you look deeper than that “headline” discount number.

Start with PIMCO itself. I’ll admit I’m a big fan of the company. Founded by legendary investor Bill Gross in the ’70s, it has an ironclad hold on investors’ imaginations, which is why its funds almost always trade at premiums.

The numbers back that up. From 2000 to 2009, Gross netted 7.7% yearly for his investors—a big return from bonds—earning himself the Fixed Income Manager of the Decade title from Morningstar.

Gross was deposed from PIMCO and replaced by Dan “the Beast” Ivascyn, who nabbed Fixed-Income Manager of the Year honors in 2013 and was inducted into the Fixed Income Analysts Society Hall of Fame in 2019.

Which brings me back to PTY’s “discount in disguise.” As I write this, the fund’s 16.8% premium is, with the exception of the April “tariff terror,” the lowest it’s been in more than two years, and well below its five-year average of 23%

PTY Is Cheap, With “Premium Momentum”

That’s a nice setup for us—a premium that’s below its trend line but moving back up.

Ivascyn’s team has spread the portfolio across US high-yield debt (38%), emerging markets (14%) and non-US developed markets (15%). The other roughly 33% is in non-agency mortgage-backed securities, investment-grade bonds and other loans.

There’s a lot to like about this split, as the fund’s US bonds stand to gain as rates fall. As for its non-US holdings, they get a couple other tailwinds:

- They benefit as US investors look abroad for higher yields, and …

- These foreign holdings catch US investors’ attention as the interest they pay in their currencies translates into more greenbacks as the US dollar falls (more on that below).

Moreover, the fund’s relatively long effective maturity (around seven years) is a nice kicker, as longer-dated bonds are especially attractive as rates fall.

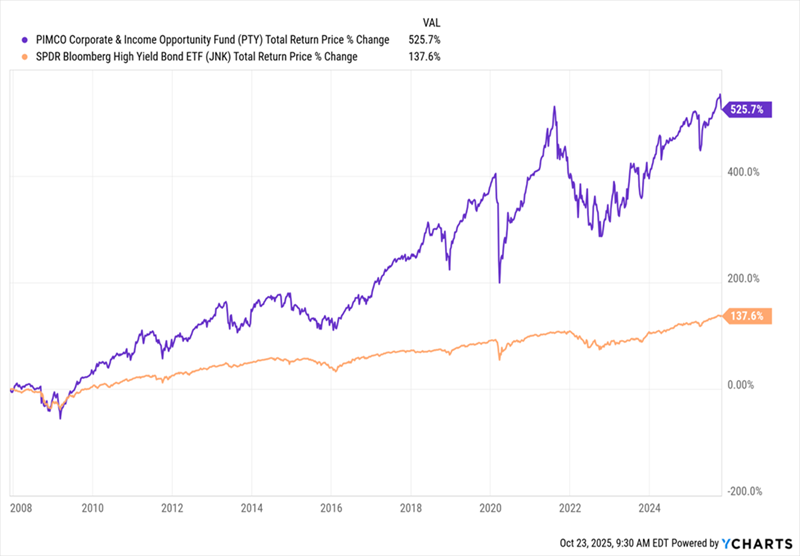

In the long haul, it’s tough to argue with PTY’s performance. The fund has been around since 2002, longer than the benchmark US corporate-bond ETF, the SPDR Bloomberg High Yield Bond ETF (JNK). In the years since JNK’s launch, it’s clobbered that benchmark. It’s no contest!

PTY Laps JNK—Again and Again

What’s more, reinvested dividends drove pretty well all of that return, thanks to PTY’s huge monthly payout.

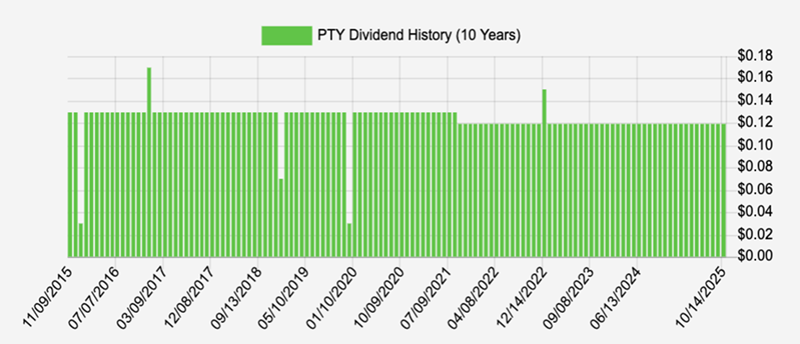

A 10.3% Yield We Can Bank On

Despite a slight reduction during COVID, this fund’s payout has been holding steady for years. And besides, its regular special dividends (the spikes and dips above) have gone a long way toward making up for that cut.

With Bessent likely to keep his thumb on rates, we can expect a floor under this rich payout, too, making PTY worth a look now.

A “Bonus” Pick to Cash In on a Lower Greenback

Let’s come back to the dollar, which has plunged this year and is likely to fall further with rates.

One way to take even greater advantage of that is through the Templeton Emerging Markets Income Fund (TEI), which states straight out that it holds “local currency positions [emphasis mine] in specific emerging and frontier markets that we view as having attractive risk-adjusted yields.”

As you’d expect from an emerging-market fund, TEI holds most of its corporate and sovereign bonds in the Middle East, Africa, Latin America and the Caribbean. Its dividend—current yield: 9.2%—also rolls in steadily and monthly.

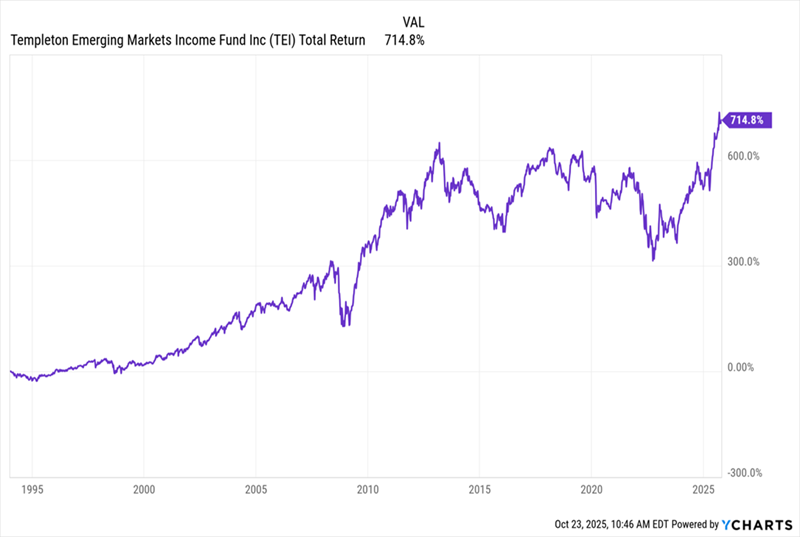

The fund has also been around since 1995 and has posted an impressive return in that time, to the tune of 715%:

TEI Drives Steady Gains From a Volatile Sector

The only thing that makes me hesitate about TEI now is its discount: at 6.6%, it’s narrower than its five-year average of 8.8% and pricier than it was at the start of the year, when it was around 9.5%.

That makes TEI second-fiddle to PTY, which you could see as an “all-in-one” US and international bond play (with a higher yield, to boot).

My Top Pick as Rates Fall? This GROWING 11% Divvie

TEI and PTY are great funds, but they’re just a warm-up for the bond fund I’m going to spill the beans on right here.

This one, which is my No. 1 high-yield bond pick now—yields more than the two CEFs above: a monster 11% yield.

Plus it pays dividends monthly and is cheap, too.

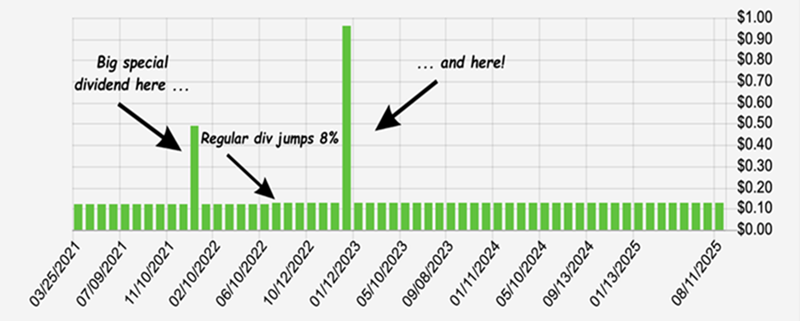

Here’s the kicker: Its 11% payout is GROWING. Special dividends? Yep. They drop on the regular, as well:

One of the Biggest Monthly Dividends I’ve Ever Seen—and It’s Growing

This one is, hands-down, my top buy as Bessent keeps massaging rates lower, not least because it has three ways to pay us:

- With its huge 11% dividend

- Through dividend growth

- Through price gains, as its discount closes and rates remain capped (or fall).

The time to buy this one is now, and I don’t want you to miss out. Click here to learn more about this life-changing 11% dividend and download a free Special Report revealing its name and ticker.