There is a massive desire for consumers to get back to traveling. If you’ve been to an airport lately, the only big change is that people are wearing masks; the crowds are on par with pre-pandemic levels.

And while workers are still enjoying the WFH benefits, when it comes to leisure activity, there is a huge desire to get out of the house and spend on experiences.

Although leisure travel has rebounded nicely, business-related travel has lagged behind; technology- hello Zoom (ZM) – has helped displace a lot of the expensive and often unnecessary travel expenses.

The newer wrench into the situation comes from the Delta variant, which CDC officials say is now as contagious as the Chicken Pox. Thus, making a prediction of any sustained rebound in travel is much more difficult.

On nearly every travel-related earnings call I’ve listened to, there is some sort of warning regarding the Delta variant, however, no one is making any predictions as to what the ultimate impact might be.

“Obviously, the Delta variant and its impact on travel demand for the fall is hard to forecast today, but we have not seen or experienced any notable declines in booking trends or cancellations so far.”

– Jon Bortz, CEO, Pebblebrook Hotel Trust (PEB), Q2, 2021 Earnings Call

Consumers that were considering booking a lengthy vacation might now be rethinking that decision. And I’ve seen large conferences pushed back due to concerns about local Delta variant spread.

But, with uncertainty comes opportunity. If we want to make money, we need to grab that uncertainty by the horns and try to profit from it.

“Every decade or so, dark clouds will fill the economic skies, and they will briefly rain gold. When downpours of that sort occur, it’s imperative that we rush outdoors carrying washtubs, not teaspoons.”

– Warren Buffett, 2016 Letter to Shareholders

The Hotel REIT market is one area I’ve been focused on to try to potentially capitalize on this uncertainty.

As a background and a quick refresher, Hotel REITs are highly capital-intensive businesses. The hotels you might be familiar with such as Marriott (MAR) and Hilton (HLT) are asset-light operators and don’t usually own any of the hotels you stay in.

Hotel REITs own the hotel and contract with operators such as MAR and HLT to help manage the property. For example, Host Hotels (HST) has a portfolio of high-end hotels, many with the Hyatt and Marriott brand name. HST pays a royalty fee for the naming rights, along with a recurring revenue stream based on a percentage of room revenues.

So, with HST, you are buying into the ownership of a portfolio of hotels, whereas with a MAR, for example, you are buying into the overall brand and management’s ability to effectively grow profits based on further expansion of the Marriott brand name.

Now, there are a few important industry stats that we need to be aware of when trying to get a good grip on the overall Hotel REIT market.

First, let’s start with overall travel industry trends to see where we might be in the travel cycle.

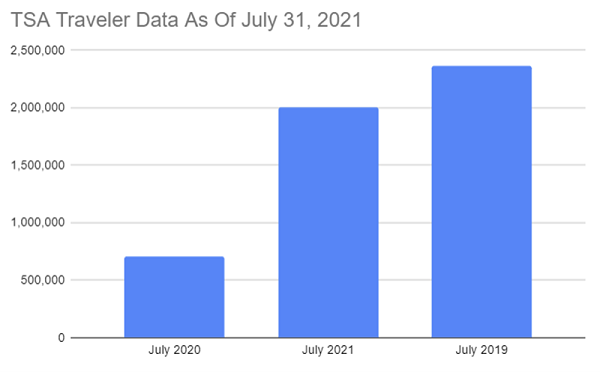

In looking at the latest TSA Checkpoint data, it’s clear that activity is brisk; current data shows that we are now at 85% of July 2019 pre-pandemic flight activity, a HUGE improvement from only a year ago, when we were at 30% of July 2019’s totals.

Source: TSA.gov

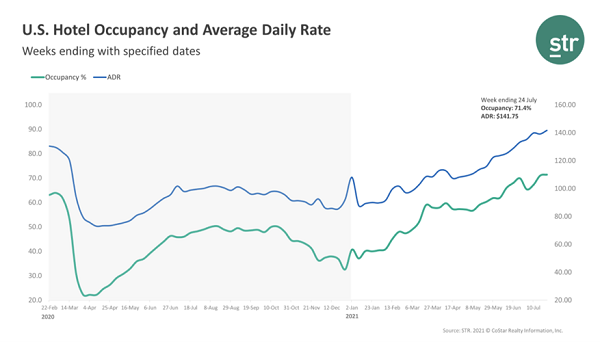

To get a gauge of hotel activity, we need to pay attention to occupancy rates (what percentage of the hotel is booked), the Average Daily Rate (or ADR-what are customers paying for a room), and RevPar (or revenue per available room). Given the depressed levels of 2020, it’s best to compare to pre-pandemic levels from 2019.

Here we can see that occupancy rates and average daily room prices have slowly been increasing from the pandemic lows in early 2020.

Recent occupancy rates hit 71%, which marked the highest level since 2019, and room rates hit an all-time high. It should be noted however that this recent summer period is typically the highest for the full year due to summer travel.

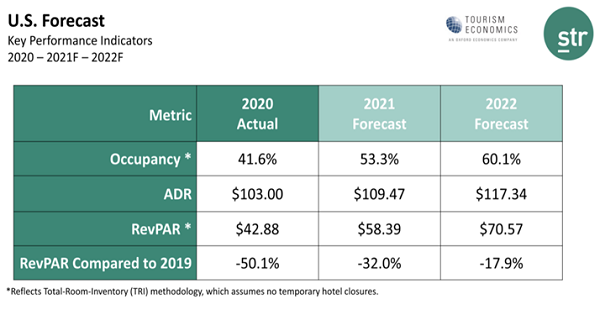

Forecasts from STR and Tourism Economics predict full-year occupancy rates for 2021 to reach 53.3% which is a big improvement from 2020, but still below the average of about 66% in recent years.

And STR expects that we still have some work to do in relation to business/group travel:

“Leisure travel demand is gathering strength with substantial recovery in sight for many markets. However, transient business, group and international travel face continued headwinds, and a full recovery will take several years.”

– Adam Sacks, Tourism Economics

So how do we play this as investors?

Let’s look at three Hotel REITs that I think are good opportunities here.

One quick note is that there are only a few Hotel REITs that are still paying dividends, and even still those payers are minuscule at the moment.

At the height of the pandemic, these hotel owners were forced to slash costs and the dividends had to go. Thus, the hope, with any of these investments, is that once operations can stabilize and return to normalcy, the dividend should come back at some point.

Hotel REIT Pick No. 1: The King Of Luxury

Host Hotels & Resorts (HST) is a real estate investment trust that owns what I would consider the cream of the crop hotel properties. These include various resort and destination hotels, many under the Marriott, Hyatt, and Ritz Carlton brand names. The company’s portfolio is concentrated in urban and resort destinations, with the former being a drag on recent results due to slowed business travel.

And the strength of their balance sheet (HST is the only investment-grade Lodging REIT) has led to management being able to capitalize on the weakness of other competitors as it recently acquired two premium properties-the Hyatt Austin and the Four Seasons At Walt Disney World at attractive prices.

Its stock has recovered from pandemic lows but still trades well below pre-pandemic levels.

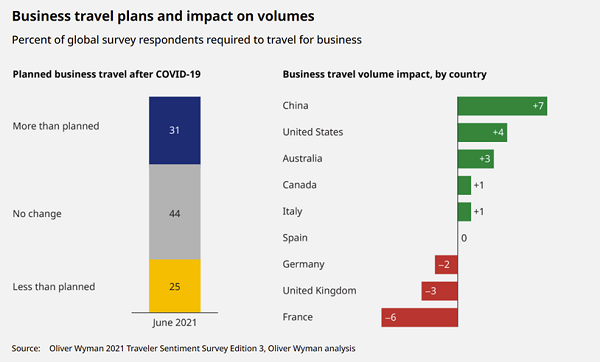

HST is certainly tied to a hopeful business and group travel recovery. Recent data trends show improvements – a survey by consulting firm Oliver Wyman showed that 76% of survey respondents planned to travel for business in the next three months, with many concerned about the ‘fear of missing out on a major deal’.

And recent results show an improvement in group demand; HST noted in its recent earnings call that it has 1.2 million group rooms booked in the second half of the year, which is up approximately 20% since the first quarter. Another positive – over two-third of the group room nights booked in the second half of 2021 were booked in Houston, Boston, New York, and Denver, urban areas that have been slower to recover.

HST in recent years has averaged between a 4% to 5% dividend yield and while it doesn’t pay a dividend at the moment, I would expect they will be amply equipped to cover a dividend as operations improve.

Its current valuation at 19x forward FFO looks attractive and is about a 20% discount to its historic five-year average.

HST is my favorite pick for any investor looking for a portfolio of premier high-class luxury hotels leveraged to a turnaround in business travel.

Hotel REIT Pick No. 2: Conventional Wisdom Says This One Should Work Well

Like HST, Hotel Real Estate operator Ryman Hospitality Properties (RHP) is heavily tied to a recovery in business travel. In fact, its primary focus is the convention segment of the hotel market, with five large convention center hotels under the “Gaylord” brand, located in Nashville, Orlando, Dallas, Denver, and DC.

Like HST, Ryman has been decimated due to a fallout in group travel and a decrease in convention center demand throughout the pandemic. However, group demand appears to be coming back.

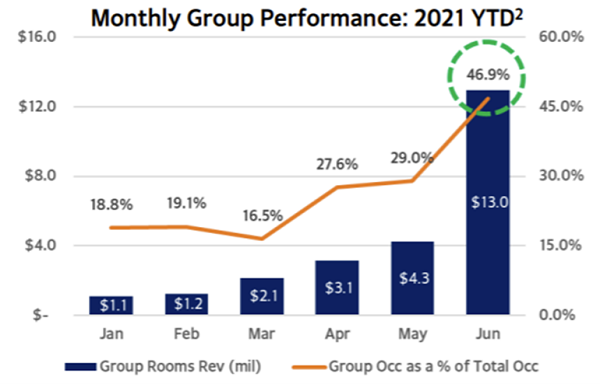

In a July investor update, RHP noted that the group revenue pace for 2022 bookings remains ahead of pre-covid levels from 2019. And June totals saw a surge in group bookings to 47% of total room nights.

Source: Ryman July Investor Presentation

One other important note for investors about Ryman; this is not just a business / convention / groups recovery play. RHP also owns a portfolio of entertainment brands and venues (which account for 11% of revenues), making it a bit more tied to “fun money” spending and not just on business travel recovery. Examples include the legendary Grand Ole Opry in Nashville, which provides a weekly showcase of country music’s finest performers, and the Ryman Auditorium, a live music venue.

Ryman doesn’t pay a dividend at the moment but recently announced that they were nearly break-even from a cash flow perspective in the second quarter and expected positive cash flow throughout the end of the year.

Pre-pandemic, RHP had posted nearly 50% growth in funds from operations (FFO) over four years, with a solid 29% growth in dividends and a steady 52% return from shares. For any investor thinking that group travel and convention activity will normalize over the next few years, RHP is the preferred play.

Hotel REIT Pick No. 3: An Apple A Day Keeps This Hotel REIT in Play

Apple Hospitality REIT (APLE) owns a whopping 232 hotels spanning 35 states with nearly 30,000 guestrooms. These properties feature the market’s most well-known mid-upscale brands across the Hilton, Hyatt, and Marriott families.

Whereas REITS such as HST and RYP are more heavily tied to a business/group travel recovery, Apple is more focused on the transient traveler with a focus on leisure. As shown in the chart below, only 13% of their business is tied to group travel.

Source: Apple Hospitality Investor Presentation

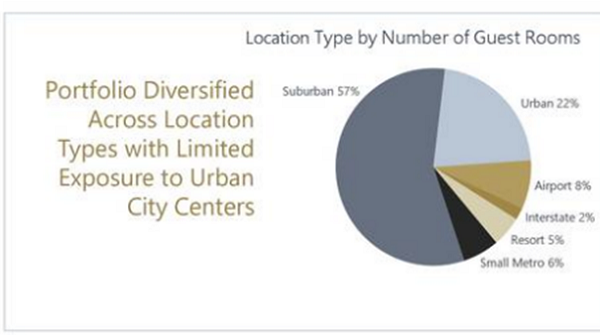

In addition, APLE has a more suburban focused footprint, as opposed to more Urban markets which have been much slower to recover:

Source: Apple Hospitality Investor Presentation

Like others in the space, APLE had to slash its dividend, although it is one of a few Hotel REITS still paying a dividend, although it’s only 1 cent per quarter.

In comparison to other competitors, from a balance sheet perspective, APLE appears well-positioned to be able to reinstate their dividend as booking activity continues to improve. Its Net Debt to EBITDA ratio has historically been well below peers, as management has been prudent in not over-levering their balance sheet.

While I like these three Hotel REITS as beneficiaries of a continued travel rebound, they don’t offer much in the form of dividend income at the moment. If it’s high dividends you’re after, Chief Strategist Brett Owens has you covered with his 7% Monthly Dividend Portfolio.

As the name says, the stocks and funds in his portfolio pay out a 7% average dividend today, and your payouts come to you every 30 (or 31) days, like clockwork!

That matches up perfectly with your bills. And if you invest, say, a $500K nest egg, you’ll pull in a tidy $2,916 a month. That’s an incredible payout in today’s world, and it could easily be enough to let you retire on dividends alone!

Don’t miss this unique income opportunity. Get the full story on this breakthrough portfolio—including the names, tickers, and his complete research on every stock and fund inside—right here.