Today I’m going to show you an easy way to use the S&P 500 Dividend Aristocrats—companies that have hiked their dividends for 25 straight years or more—to build a durable income stream you can retire on.

But before I do, there’s something I need to tell you about these 50 companies, which are “sacred cows” in many investors’ eyes: the fact they’re in this exalted club today doesn’t mean they will be in the future.

Consider ExxonMobil (XOM), a long-time Aristocrat that’s losing money fast and may be forced to slash its payout.

I know I don’t have to tell you what investors who are relying on XOM’s 3.6% dividend would do if their quarterly “paycheck” suddenly dropped in half. That’s why I recommend staying well clear of XOM today.

But that’s not all. You also need to resist the temptation to follow the herd and simply buy an ETF, like the ProShares Dividend Aristocrats ETF (NOBL) and forget about it for a decade.

Why?

Because NOBL’s dividend yield is just 1.95%—less than the S&P 500 average. And while its payouts are growing, they’re also very uneven, having gone up and down since the fund started in 2014. I don’t know about you, but that doesn’t sound like a recipe for a relaxing retirement to me.

The Best Way to Buy the Dividend Aristocrats

But don’t worry. As I mentioned off the top, there’s a smarter way to get a far bigger upfront income stream out of these dividend stalwarts—and one that grows in a stable, predictable way, as well.

You do it by zeroing in on the Aristocrats boasting the highest dividend yields, in addition to strong free cash flow.

If we did this, we’d end up buying HCP Inc. (HCP), AT&T (T), and Emerson Electric (EMR). These three stocks give us a high 4.8% yield as of this writing and payouts that will only grow in the future.

It’s a good start, but I’m going to add two more stocks to make the portfolio even more diversified. The first is Procter and Gamble (PG), which is currently yielding 3.1% and has a long history of dividend growth.

PG isn’t one of my favorite dividend stocks, but it tends to outperform during recessions, giving us a bit of downside protection. It also has a dominant position in emerging markets, so we get some exposure to developing countries, as well.

On top of that, I’m going to add Verizon (VZ) and enjoy its 4.9% dividend yield.

“Wait a minute,” you’re probably thinking. “Aren’t we already buying AT&T? Why hold both of the main telecom companies?”

Because even though they’re in the same industry, they’re evolving into very different businesses. And for that reason, I want them both.

AT&T, for example, aims to keep investing in top-quality TV content by acquiring Time Warner (TWX), while VZ is pinning its future to online growth by through its purchases of AOL and Yahoo (YHOO).

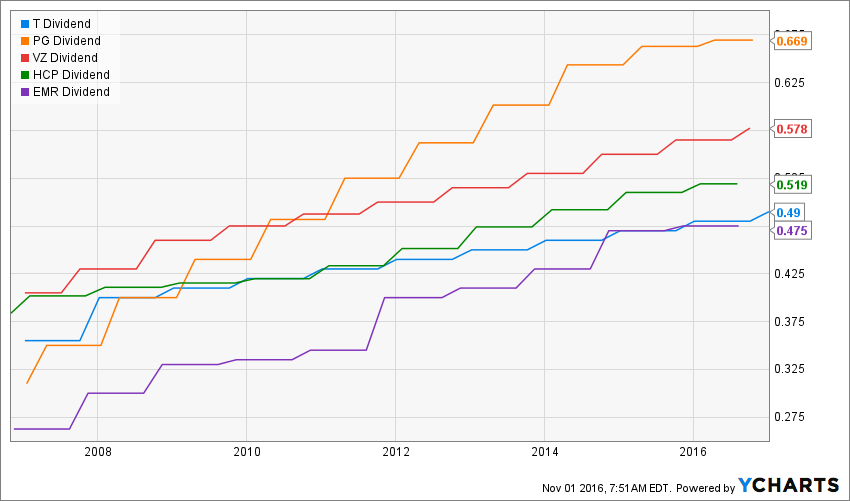

Now that we’ve built our five-stock Aristocrat portfolio, let’s look at how its dividends have grown over time.

A Stairway to a Comfortable Retirement

This Steady Eddie payout growth is exactly what these firms’ investors expect. And each company has lots of free cash flow (FCF) available to cover its dividend payments, so we can count on those hikes continuing well into the future.

HCP, for instance, boasts an FCF payout ratio of 66%, while AT&T’s is 67%—meaning both have nearly a third of their cash flow available for dividend increases. And that’s to say nothing of the higher cash flow that will inevitably spring from their expansions and efficiency improvements.

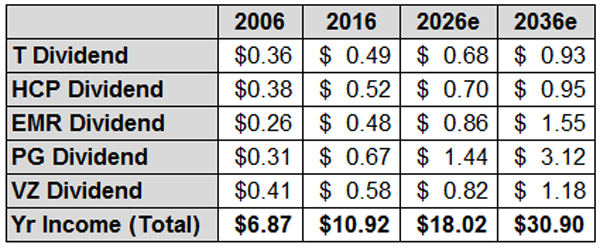

So I think we can safely say that further payout growth is a lock—and a deeper look into the numbers shows just how much growth we can expect:

Boring Companies, Exciting Dividend Growth

From here, we can see that our annual income goes up by 65% in a decade and a whopping 183% in two decades! This just shows how patient investors pocket more and more income over time.

But there’s more to the story.

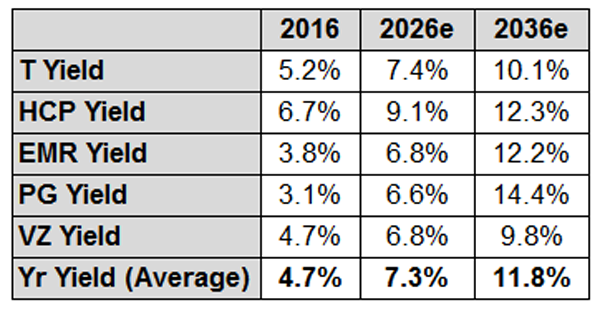

If we look at the yields of these stocks today, we see a portfolio with a current yield of 4.7%. But look at what’s likely to happen to the yield on your initial buy over the next 10 and 20 years:

More Income to Those Who Wait

Note that these yields are based on 2016 share prices—and since these stocks will likely go up over time, there will be capital gains we’re not taking into account here.

We’re also not looking at dividend reinvesting (yet—read on for that), so this is a simplified picture that underestimates the income reality.

And what a reality it is—by buying and holding for a decade, we go from 4.7% income to 7.3%, then up to 11.8% in 20 years!

Let’s put that in real dollars and cents. If you have $500,000 now and invest in these dividend-growth stocks, you’ll generate $23,460 in pre-tax income this year … not yet enough for most people to quit working.

But in a decade, your income stream will be up to $36,700—and that might be enough for you, depending on where you live. In another decade, you’ll have a nice $58,850 in annual income, which tops the median household income in America today. That’s surely enough to comfortably retire in many parts of the country.

Your Secret Weapon Against Inflation

But this is only half of the story. What about inflation?

Let’s assume we get the same inflation rate over the next 20 years as we’ve had over the last decade. That means we’ll have to spend $1.20 in 2026 to get $1.00 worth of stuff in 2016.

So in a decade, that $36,700 will be more like $30,583 in today’s dollars. Similarly, the $58,850 in 2036 is more like $40,868 in 2016 money—still a comfortable living, especially if you aren’t paying to commute to the office, buy coffee and lunch and so on.

And remember when I mentioned dividend reinvestment earlier? Here’s where it comes in.

If we start with $500,000 and don’t add any more to our retirement portfolio, we’re still going to get dividend payments from these companies until we retire. By reinvesting our dividends as they grow, we’ll juice our income stream even further.

If we do this, our portfolio will grow to be worth over $850,000 in 2026 and over $2 million in 2036.

Our yields on the invested dividends over the next couple of decades will be lower than the 7.3% and 11.8% noted above, but even if they’re the same yield as we’re getting today, that means our passive income will become about $42,000 in 2026 and a whopping $112,000 in 2036!

Even when you account for inflation, I think you’ll agree these are comfortable income streams for a retiree.

Fast-Track Your Retirement With My “No-Withdrawal” Portfolio

These 5 Dividend Aristocrats are a great way to build reliable income for retirement, but you’ll still have to wait a full decade before you’ll be yielding 7.3% on your initial buy.

Why wait that long when you can grab an 8% yield straight out of the gate with my “No-Withdrawal” retirement portfolio?

That means a $500,000 investment will kickstart a $40,000-a-year income stream, starting right now. That’s nearly double what you’d get in the next year from our five-stock Dividend Aristocrat portfolio. And you won’t have to give up capital gains and payout growth to get that high, safe yield.

As the name suggests, I’ve built this portfolio so you won’t have to tap any of your capital whatsoever, no matter what happens with the markets after you retire. If there’s a meltdown, you can just kick back and keep collecting your dividends till things settle down again.