If you’re sitting in “dead money” Treasuries and CDs, the dawn of a new round of interest-rate cuts is probably the last thing you want to hear.

Since Federal Reserve Chair Jerome Powell’s “pivot” on rates in early January, the yield on the 10-year Treasury has plunged, from 2.7% to 2.0%.

So if you put a million bucks in Treasuries at the start of the year, you’d be banking $26,900 in income. That’s pathetic enough for a seven-figure nest egg!

But fast-forward just six months, and your mil fetches you far less: just $20,100.

Powell Will Spark a Stampede Into These 8% Dividends

With Treasury rates collapsing and the stock market soaring—driving S&P 500 dividend yields down to a lame 1.7%—there are few places for income-seekers to turn.

Note that I said “few,” not “none.”

Because Powell’s pivot is sending folks scurrying into another corner of the market, closed-end funds (CEFs), which are renowned for sky-high dividends of 8% and up.

That’s the difference between a paltry minimum-wage income of $20,100 on a million saved or a respectable $80,000 annually.

And because CEF investors react more slowly than your typical stock buyer, there are still bargain-priced CEFs out there, even with this year’s big market run-up.

But CEFs tend to be more nuanced than buying stocks, because we’re evaluating managers and (sometimes shifting) strategies, rather than established business models. So today I’m going to give you five strategies I personally use to find the biggest (and safest) dividends in CEF-land, with the most price upside ahead.

Let’s get going.

CEF Strategy #1: Price Charts Can Deceive

The Gabelli Dividend & Income Trust (GDV) has been a great performer in the last decade—but going by its price chart, it looks like anything but, badly trailing the “dumb” SPDR S&P 500 ETF (SPY), which blindly tracks the market:

GDV’s Price Chart Would Worry Any Investor …

But remember that CEFs are income vehicles (GDV, for example, pays a nice 6.2% dividend as I write). That means a simple price comparison doesn’t cut it: we need to add dividends back in to get the complete picture:

… But Dividends Make the Difference

As you can see, with dividends included, GDV, beat the market in the last decade, at many points by huge margins. It gets better: because of the fund’s high yield, most of this return was in cash, not the “paper” gains SPY investors received.

The key takeaway: make sure the chart you’re reading includes dividends paid (so it reflects total returns).

CEF Strategy #2: Go Beyond the Dividend Yield

A fund’s history can tip you off to the quality of the management team and its strategy. GDV has one of the smartest stock pickers on the planet in Mario Gabelli, who drove it to that monster 294% return—again, mostly in cash.

But not all CEFs have that kind of high-powered management, so you need to look past the headline dividend yield and focus on dividend stability and past performance. After all, a high yield isn’t going to do you much good if the fund’s share price drops out from under you.

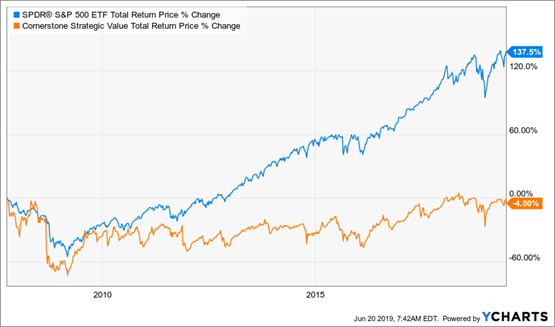

That’s precisely the “dividend trap” awaiting the folks who heed the siren call of the absurd 21% dividend on the Cornerstone Strategic Value Fund (CLM). Its management team has delivered the worst of all worlds, with the fund crashing harder than the broader markets in 2008 and never recovering.

In fact, CLM’s share price has dropped 91% since the pre-crisis peak in October 2007!

Share Collapse Snatches Away Dividend Payouts

And adding CLM’s dividend back in still doesn’t get investors’ heads back above water.

Dividends Can’t Push CLM Into the Black

Don’t be drawn in by CLM’s 21% yield—as we just saw, it’s not going to do you much good when the fund’s share price collapses under you.

Which brings me to our next point…

CEF Strategy #3: The Best Way to Spot a Looming Dividend Cut

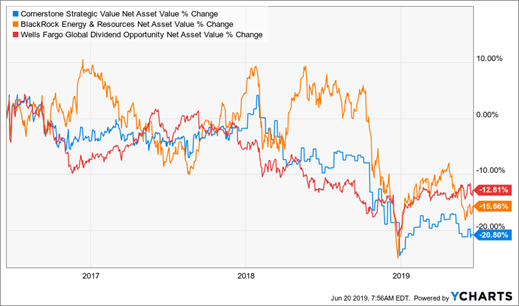

One way to tell if a CEF’s payout is a “sucker yield” like CLM’s is to look at how management funds their payouts. And luckily there’s a “one-click” way to do that: check out your fund’s net asset value (NAV, or the market value of a CEF’s underlying portfolio).

Because the one thing you don’t want to see is a CEF making its dividend payouts by eating into NAV. Here’s a look at what CLM’s NAV has done in the last three years, plus two other funds whose big yields are built on flimsy foundations:

These Big Dividends Have a Terrible Secret

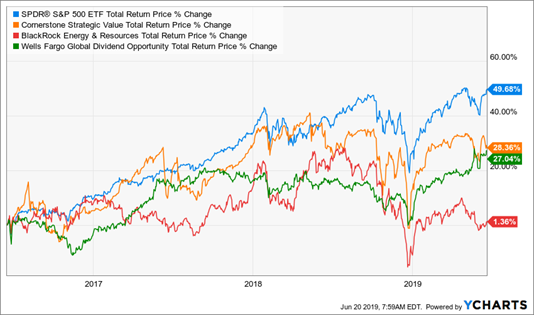

As you can see, CLM, plus the BlackRock Energy and Resources Trust (BGR)—in orange—and the Wells Fargo Global Dividend Opportunity Fund (EOD)—in red—have all seen terrible NAV performance in the last three years.

So even though this trio offer outsized dividends of 21%, 8.2% and 11.2%, respectively, that hardly matters! Because all three funds’ weak NAVs kneecapped their total returns (with dividends included). You would have been way better off just buying SPY (shown in blue below) and being done with it!

Poor Management Crushes Returns

The bottom line? Always check out a fund’s NAV performance, in addition to its market-price return and dividend history, before clicking “buy.”

CEF Strategy #4: Use This Trick to Buy Below Cost

One aspect of the CEF structure lends itself perfectly to contrary-minded investing: fixed pools of shares.

Mutual funds issue more shares whenever they want. But CEFs have a fixed share count, with their funds trading like stocks. As a result, from time to time a fund will fall out of favor and find its shares trading at a discount to its NAV.

This is basically free money because these underlying assets are constantly marked to market. If a fund trades at a 10% discount, management could theoretically liquidate the fund and cash out everyone at $1.10 on the dollar. Or it can buy back its own shares to close the discount window (and boost the share price).

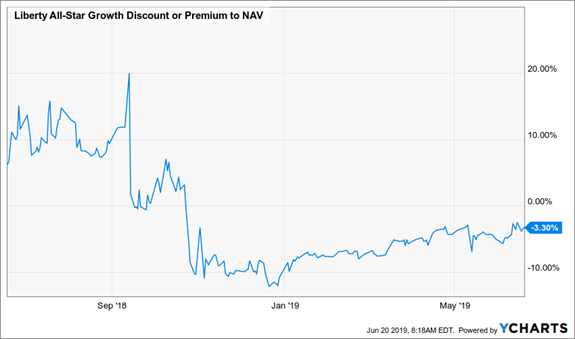

It’s also important to put the current discount in context.

For example, the Liberty All-Star Growth Fund (ASG) trades at a 3.3% discount now. That doesn’t sound like much, but the fund has traded at massive premiums over the last year (up to 20%!), implying some very nice upside here:

ASG: A Deal in Disguise

Just before I sign off, we need to discuss one other thing about CEFs that scares most investors, but really shouldn’t.

CEF Strategy #5: High Fees Can Be a Plus

Most investors are conditioned by their experience with ETFs to search out the lowest fees. This makes sense for investment vehicles that are roughly going to perform in-line with the broader market. Lowering your costs minimizes drag.

Closed-ends are different, though. On the whole, there are many more dogs than gems. It’s an absolute necessity to find a great manager with a solid track record. Great managers tend to be expensive, of course, but they’re worth it.

The stated yields you see quoted, by the way, are always net of fees. Your account will never be debited for the fees from any CEF you own. They are simply paid by the fund itself from its NAV.

Urgent Bulletin From the Publisher

I’m Kevin Wallen, the publisher here at Contrarian Outlook.

I don’t normally break in on Brett’s articles, but I feel I must do so today, because something unprecedented just happened at our CEF Insider service.

If you’re in the market for high-yield CEFs (and the fact that you’ve read this far tells me you may be), this is great news for you. Because what I’m about to tell you can set you up for safe dividends up to 10.7%, plus fast 20%+ price gains!

I’m talking about the latest critical buy alert from CEF Insider’s proven fund-picking system, which, frankly, shocked all of us here at Contrarian Outlook.

Why?

Because this finely tuned setup just dropped 4 straight 8.7%+ yielding picks on us.

That’s unprecedented: CEF Insider strategist Michael Foster has this fund-picking formula so tightly programmed that it rarely produces even one recommendation, let alone 4 in quick succession!

Here’s what this extraordinary critical buy alert means for you:

- These 4 “ironclad” CEFs yield 8.7%, on average, and one of these cash machines even throws off a safe—and growing—10.7% payout. Plus …

- Thanks to their massive discounts to NAV, we’re looking at 20% price upside in the next 12 months, too!

I can’t wait to show you these 4 cash-spinning picks. All you have to do is click here and Michael will give you their names, ticker symbols, best-buy prices and his very latest analysis of each and every one.