What’s better than an asset class that can deliver 8% in annual income like clockwork? How about one that’s actually poised to pop as interest rates rise?

And oh by the way, this industry lets us invest like privileged private equity investors. No “seven-digit” buy-in needed here though! We buy these dividend machines just like we would any other stock.

That might sound too good to be true, especially when we consider that stocks broadly still yield less than 2%. But we’re simply talking about an underappreciated area of the market that includes only a few dozen stocks or so.

Let’s talk about three of these payout powerhouses today. The trio yields a nifty 9.6%. But first, a quick primer on the “dividend loophole” these firms take advantage of (perfectly legally).

BDCs: Private Equity for the Rest of Us

You might be aware that, back in 1960, Congress created real estate investment trusts (REITs) to open up real estate investing to the masses.

But that wasn’t the only high-yield vehicle Washington put into play.

Two decades later, Congress willed another business entity into existence—business development companies (BDCs for short), which were meant to help provide much-needed capital to America’s small and midsized businesses.

For years, larger banks had largely turned up their noses to smaller businesses, which were rife with risk. And on the rare occasion they would provide financing to these budding upstarts, they’d charge them through the nose for the privilege. BDCs were the answer to this financing vacuum.

Now, like private equity, business development companies provide all sorts of debt, equity and other financing to firms in countless industries. As a result, BDCs boast diversified portfolios of private businesses that none of us could invest in on our own. But unlike PE, which typically requires investors to ante up a million or so to play, you and I can jump into a BDC for the price of a single share—typically between $10 and $100.

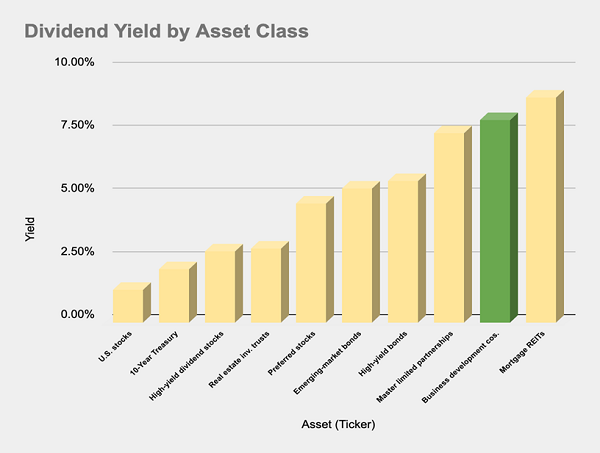

It can be a growth business, but where BDCs really shine is on the dividend front. That’s because, like their older REIT cousins, BDCs can take a pass on paying federal taxes as long as they put 90% of their taxable income back into the hands of shareholders. Indeed, BDCs are one of the most impressive sources of income on the market:

BDC Income Dwarfs Most Other Asset Classes

One last bonus: Many BDCs deal heavily, if not exclusively, in floating-rate loans, which makes them perfect for today’s specific challenges. Because as benchmark interest rates rise, so too do the rates on BDC loans—translating into wider margins and fatter profits.

Let’s be clear: Business development companies aren’t without their challenges. Because they invest in privately held businesses, BDCs’ portfolios can be extremely opaque and nearly impossible to evaluate. It’s also a cutthroat industry—one in which BDCs have been forced to compete with a growing number of financing providers.

Still, those seeking truly superior yield would be hard-pressed to do better than these mega-sized payouts:

PennantPark Floating Rate Capital (PFLT)

Dividend Yield: 8.7%

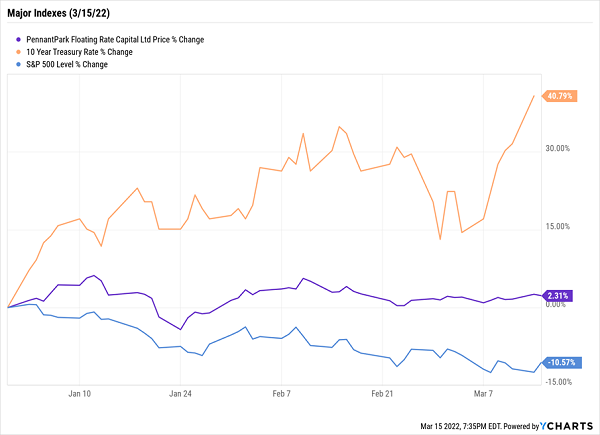

In September 2021, the last time we explored PennantPark Floating Rate Capital (PFLT), things weren’t going well for the virtually exclusive provider of floating-rate loans. That’s because interest rates were headed sharply in the opposite direction—after a recovery in rates across the first quarter or so of 2021, the 10-year T-note was back to plumbing 1.2%-1.3% by late summer.

Indeed, several Wall Street analysts who cover the stock were worried about PFLT’s ability to cover its gigantic monthly dividend.

Fast-forward about half a year, and things are looking dramatically different.

A quick refresher: PennantPark Floating Rate Capital primarily invests in companies owned by established middle market private equity sponsors that typically support their portfolio companies. Portfolio companies typically generate $10 million to $50 million in annual earnings before interest, taxes, depreciation and amortization (EBITDA).

The BDC currently boasts 115 portfolio companies in 46 different industries—business services, government services, healthcare, software and other sectors that typically deliver steady cash flows. The vast majority of its investments (87%) are made through floating-rate first lien senior secured debt, with preferred and common equity accounting for virtually all of the rest.

In a very short amount of time, PFLT’s floating-rate portfolio has gone from burden to boon.

Pennant Isn’t Balking at Booming Bond Yields

The BDC also enjoyed a lift after fourth-quarter net interest income (NII) came out much better than expected, on the back of brisk investment activity—originations were more than double some expectations. It also upped its investment in a joint venture with a Kemper (KMPR) subsidiary.

A more aggressive PennantPark and a friendlier interest-rate environment have analysts far more optimistic about PFLT’s ability to keep writing its dividend checks. That makes it a far safer play—at least as long as the hawks are in charge at the Fed.

Hercules Capital (HTGC)

Dividend Yield: 11.3%*

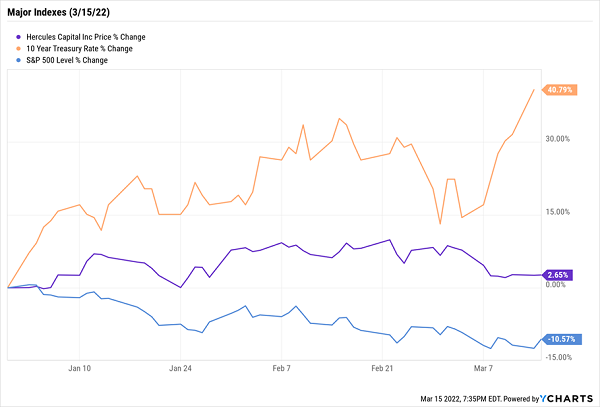

Hercules Capital (HTGC) is a little more focused than PennantPark, choosing to invest in cutting-edge technology: that’s not just tech businesses, but also the life sciences, sustainable and renewable industries.

To date, HTGC has funded more than 560 companies, including over 230 exits via initial public offerings (IPOs) and mergers and acquisitions (M&A). The firm boasts $13 billion in commitments since December 2003, and has $2.6 billion in assets currently under management.

The portfolio currently includes companies such as:

- 23andMe, a consumer DNA genetic testing company

- Postmates, an online delivery and pickup services app

- Bicycle Therapeutics, a biotechnology firm seeking out treatments for diseases that are underserved by existing medicines

HTGC is built for the moment. More than 90% of its investments are in debt, and 94% is floating rate in nature. That has helped keep Hercules aloft while the broader market drifts lower.

Hercules Stays Strong Through the Downturn

That, as well as extremely high credit quality, should give income investors peace of mind about their paychecks.

So too should management’s stewardship of the dividend. That is, the company pays a regular quarterly dividend—a hefty one that guarantees a 7.8% annual yield—but adds special cash dividends as profits allow. Indeed, Hercules paid out special dividends every quarter last year, and if it does the same this year, its 15-cent special payout annualizes to another 3.5%, good for mouth-watering yield of more than 11%.

Just don’t ignore the price tag. HTGC shares currently go for 1.5 times its net asset value—one of the highest prices in the BDC space.

Owl Rock Capital (ORCC)

Dividend Yield: 8.7%

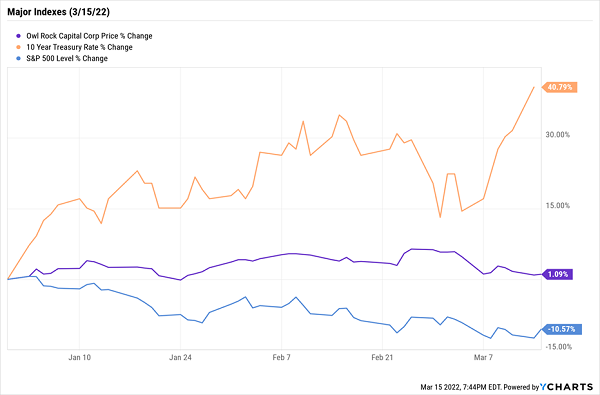

A much more reasonably priced BDC is Owl Rock Capital (ORCC), which currently trades slightly under NAV and has been weathering the 2022 market downturn like a champ.

Owl Rock Is Steering Clear of Turbulence

Small wonder there: Floating-rate investments make up 99% of ORCC’s portfolio.

Owl Rock invests in sponsored and non-sponsored U.S. middle market companies, typically with annual EBITDA of between $10 million and $250 million and annual revenues of $50 million to $2.5 billion at time of investment. Some 90% of the portfolio is senior secured; 75% is first-lien.

The largest industry concentration is just internet software and services at 11% of assets, followed by insurance (9%), financial services (8%) and healthcare providers and services (7%). As a whole, this is a fairly defensive portfolio that should not only ride out rate hikes with ease, but is better positioned than most to withstand a recession, should that come.

ORCC has a short trading history, having only gone public in 2019, and it started out offering both quarterly and special dividends like Hercules. Unlike Hercules, however, those special dividends dried up after 2020 and haven’t yet come back. But projected NII is more than enough to cover the payout, so keep an eye out—if conditions keep swinging in Owl Rock’s favor, it might be able to sweeten the pot.

Sky-High Dividends You Can Count on for DECADES

The market’s recent downturn hasn’t done investors many favors, but it has had at least one screaming benefit:

It has momentarily nudged some of the market’s best high-yield dividend names back into “BUY NOW!” territory.

My “Perfect Income” portfolio features some of the most generous, yet stable, dividend investments you can find. The only problem: In normal market conditions, they tend to trade at lofty valuations thanks to their clear performance potential. But every now and again, when the market throws a fit, Wall Street throws the baby out with the bathwater and gives us a chance to buy even more on the cheap.

And right now is one of those rare times.

Some readers have told me that the stocks in my “Perfect Income” portfolio have doubled and even tripled the dividends they were earning from their old income portfolios.

That alone is a massive upgrade to any set of retirement holdings. But more important is that my Perfect Income Portfolio delivers that level of cash while also…

- Paying those dividends consistently, predictably and reliably.

- Surviving, even thriving, in market crashes.

- Delivering double-digit returns across several safe investments.

- Gambling your hard-earned nest egg on flimsy day-trading strategies, options contracts or penny stocks.

Let me show you the stocks and funds you need to stabilize your retirement. But more importantly, let me reveal this incredible strategy and show you how to be a better investor in the process!

Take control of your financial legacy today. Let me show you how to get 2x to 4x your current income with this simple, straightforward system. Click here to get a FREE copy of my Perfect Income Portfolio report, including tickers, dividend yields, full analyses of each pick … and a few other bonuses!