The hunt for bond proxies is in full swing – but how good are these untested replacement players?

A 100% dividend-only income stream is the goal of any responsible “no withdrawal” retirement portfolio. Which of course is superior in every way to the fatally flawed 4% retirement myth, but difficult to achieve in a world where payout yields have been bid down towards 2%.

Fortunately, there are still a few promising pockets for income investors. I’m talking about yields of 6% to 8% plus upside. We’ll review them in a minute – but first, let’s make sure we avoid the high-risk low-reward traps.

Consumer “Staples” are Dangerous Reaches for 2-3%

Long term, I’m concerned that the dividend aristocrats of today will become the dividend disasters of tomorrow. For now, I worry that investors are buying high – and will eventually be forced sell low.

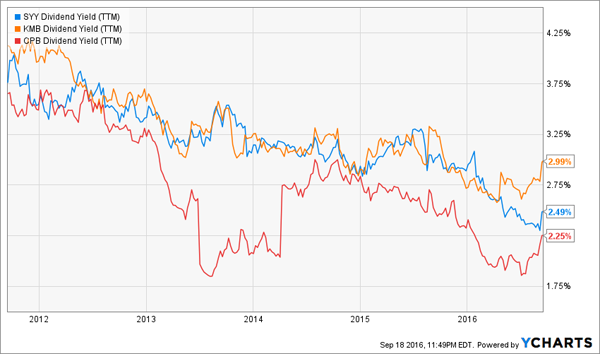

Why sell ever? Because payout percentages have been bid down to almost-meaningless levels. Take Sysco (SYY), Kimberly Clark (KMB) and Campbell Soup (CPB) – profits have been grinding sideways, yet yields are just off five-year lows:

Making a Dividend-Only Income Stream Impossible

When a million bucks won’t even fetch $30,000 in dividends, you’ll be forced to sell stock to compliment your income. Problem is, these stocks have rich price-to-earnings (P/E) ratios:

Nosebleed P/E Ratios for “Staples”

I say staples tongue-in-cheek because many consumers are now falling in love with someone other than their favorite brand, calling into question the breadth and depth of these (probably) overrated competitive moats. Odds are these P/Es will be lower when you need to sell, which means you’ll fall victim to reverse dollar cost averaging.

Remember the benefits of dollar cost averaging that built your retirement portfolio? This is the same phenomenon, but in reverse!

At sub-3% yields, moats or not, consumer staples simply aren’t going to provide enough income. At P/E ratios above 25, they are dangerous to your capital. Let’s move on to a slightly better alternative.

Utilities: At 4%, Makes Sense if You’re Rich

These traditional safe havens suffer from the same problems: popularity, and lack of alternatives. With a 3.3% yield, the Utilities Select Sector SPDR (XLU) pays more, and blue chip names like Duke Energy (DUK) and Southern Company (SO) pay a bit higher yet at 4.2%:

Multi-Year Yield Lows Here, Too

Better yields are one edge over our aforementioned pricey brands – another is safety. Even in 2016, utility customers have less alternatives available than do consumer buyers (who scarily do have a wide array of purchasing options today).

Utilities may still be a viable income option if you have, say, $5 million or more. Dividend growth is very slow in the 4% payers, but the payouts themselves are secure.

So if you only need the dividends, fine. But the stocks themselves are expensive, which means I wouldn’t buy them now if you think you’ll ever need to sell later to raise capital.

A better bet would be some select cyclicals who are selling for cheap, and at least carry a bit of upside potential to boot.

Select Cyclicals Can Be Safer Than They Appear

Industrials – companies that make big physical products (often in cyclical demand) – are paying their most generous yields since the financial crisis. Their yields of 3% and even 4% or more are 50% to 100% better than the broader market.

Problem is, that’s still not enough dividend income to retire on. But when you factor in potential price upside, some firms are interesting speculations today.

I’d avoid potential dogs like Caterpillar (CAT) and Pitney Bowes (PBI) however – the former because of its exploding payout ratio (now at 164% of earnings), the latter for its evaporating business model (which relies on traditional mail).

An intriguing alternative is Deere (DE). Its profits, and shares, tend to rally with corn prices:

Buy Deere When Corn is Low

Maize has been low for a couple of years now. It’s due for a rally as farmers get frustrated by low prices and devote acreage to other crops. If this planting neglect spurs a rally in corn as it usually does, Deere shares (paying 2.9%) should follow.

But Who Wants to Risk Retirement on Corn Prices?

The dream of a full income stream from dividends is unfortunately only available to rich people today. Yields of 3% or even 4% just won’t get it done. And who wants to gamble their nest egg on corn prices anyway?

Unless, that is, we expand our search to include investments a bit too small to get much financial press. I’m not talking about small-caps per se, either – just good ol’ fashioned US-based mid-caps.

If you’re not familiar with the less popular but more profitable “B-List” of income investments, you’re missing out. These companies with market capitalizations between $2 billion and $10 billion tend to be cheaper, and have a habit of steadily outperforming their counterparts:

Mid-Caps Dominate Large and Small

Lesser-known mid-cap plays are the cornerstones of my “no withdrawal” retirement portfolio strategy. Why rely on stock price appreciation in an inflated market when there are secure, high paying dividends you can simply live off of and keep your capital intact?

You can’t find these yields in the large-cap universe. But you can in the underappreciated mid-cap world. I’m talking about secure, cash flow backed yields of 6%, 7% and even 8%. These are the types of payouts that will fund your retirement on dividends alone. Click here and I’ll explain more about my no withdrawal approach – plus I’ll share the names, tickers and buy prices of my eight favorite dividend investments (with an average 7.7% yield!).