Today I want to tell you about two hidden pitfalls that could threaten your stock returns—and four stocks that could be the first to take a tumble.

First, the pitfalls. You’ve probably heard of the first one: seasonality.

That’s the market’s tendency to outperform—or underperform—at certain times of the year. A prime example is the “sell in May strategy,” in which some investors bow out from May to October, when market gains tend to be muted.

Now the worst month for stocks—September—is nearly upon us. According to the Hulbert Financial Digest, from 1896 through 2014, the Dow Jones Industrial Average fell an average of 1.06% in September, compared to an average gain of 0.75% for all the other months.

Before we go further, let me be clear about something: I’m not for a minute suggesting you sell all your stocks in August. That’s because these patterns don’t always repeat. The S&P 500 gained 0.32% last September, for example, and if you were out of the market in September 2013, you missed out on a 2.6% gain.

However, the pattern does make now a great time to prune weak stocks from your portfolio, starting with the four overhyped names I’ll get to in a moment.

Consumer Staples Stocks: Riskier Than They Look

Here’s something else you need to be aware of, particularly if you hold blue chip consumer staples stocks like General Mills (GIS), which I recommended selling on August 1, Kraft-Heinz Co. (KHC) and Anheuser-Busch InBev (BUD): the steady drip of these companies’ sales to smaller, nimbler competitors.

In China, for example, domestic upstart Yunnan Baiyao now controls 10% of the toothpaste market, while sales pop 45% annually, according to The Economist. Meantime in America, the big consumer-products giants have seen their collective market share dip by nearly three percentage points since 2011.

And if you’ve ventured down to your local pub lately, I don’t have to tell you that the number of craft brewers has exploded.

In the crosshairs are the three consumer staples stocks below. All have seen their valuations soar to nosebleed levels this year—but their sluggish growth and lack of innovation won’t support those gaudy numbers for long. Further on, I’ll reveal a real estate investment trust (REIT) that could also be set for a big fall.

3 Consumer Staples Stocks to Sell Now

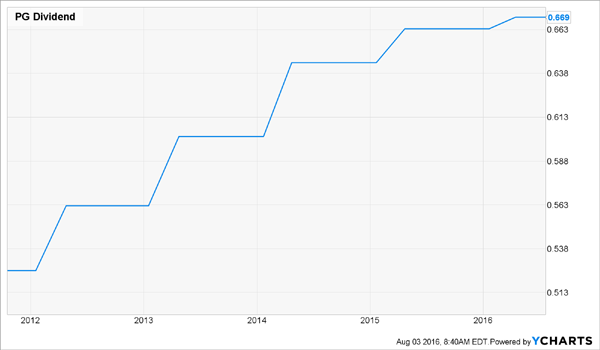

Procter & Gamble (PG) started its seemingly endless restructuring in 2012, slashing its costs by $10 billion in the process. But that still wasn’t enough: earlier this year, management said it would cut another $10 billion by 2017.

Regardless, adjusted earnings per share (EPS) dipped 15% year-over-year in the second quarter, while revenue fell 2.8%.

If P&G is going to justify its trailing-twelve-month price-to-earnings (P/E) ratio of 23, it badly needs some new blockbuster products. But if history’s any guide, it’ll be a long wait: P&G hasn’t served up anything that delivers annual sales of $1 billion or more—key to growth for a company this size—in over a decade.

Worse, management keeps buying back P&G’s pricey shares when that cash would be far better spent on R&D or rebooting P&G’s flat-lining dividend growth:

Kimberly-Clark (KMB), like P&G, is a Dividend Aristocrat, meaning it’s one of 50 S&P 500 companies that have raised their payouts for 25 straight years or more.

For plenty of investors, that alone is enough to buy. But KMB’s no bargain, either, with a P/E ratio of 24—a lofty multiple for a company that, also like P&G, is supporting earnings with cost cuts, not rising sales.

That puts it in danger of a big drop on any bad news, like what happened between April 20th and 26th, when KMB tumbled 8.7% as investors punished it for reporting sales that barely missed consensus forecasts.

Dividend growth could be in for a hit, too, due to the company’s 66% payout ratio (or the percentage of earnings paid out as dividends). The trailing-twelve-month dividend yield doesn’t offer much solace: at 2.8%, it’s close to a 12-year low and not much higher than the S&P 500 average.

Unilever (UL) boasts a P/E ratio of 24 today, near a record high. The stock dipped on July 19, when Unilever said it would buy privately held Dollar Shave Club, an online seller of razors to members for as little as $3 a month, for $1 billion.

This time, investors had it right: even though DSC is a great example of the kind of smartly run company that’s lapping the consumer-product giants, Unilever is paying five times DSC’s forecast revenue this year! That’s a huge premium for a company in the tiny, $263-million online-razorblade market. To put that in context, Unilever’s 2015 sales clocked in at $59 billion.

Sure, it makes sense to snap up a disruptor like DSC before competitors do, but here’s the problem: Amazon.com (AMZN) already offers razors for less. And there’s little to stop P&G, owner of Gillette, from joining the fray, too.

In any event, buying small, unprofitable businesses isn’t going to fix Unilever’s bigger problem: with volume growth slowing, the company is leaning on price hikes and cost cuts to support its profits—a solution it can’t rely on forever.

The 3.0% dividend yield, while better than average, isn’t enough to keep us around while management tries to navigate the shifting landscape ahead.

Dump This Pricey REIT, Too

Ventas (VTR) benefits from one of the most reliable trends out there: the retirement of the baby boomers. The company owns nearly 1,300 senior-housing and healthcare facilities, mainly in the US.

There’s no doubt this is a great business to be in. Trouble is, other investors have figured this out, too … and driven the shares up 30% year-to-date. That’s pushed the dividend yield below 4.0%.

Since investors look to REITs for income, that number doesn’t give them much reason to bid the share price higher—and it could tempt them to sell, swapping Ventas for higher yields in the senior-care space from the likes of Welltower (HCN), at 4.4% and HCP Inc. (HCP) at 5.8%.

3 Cheap REITs With Far Higher Yields Than Ventas

Even though big-name healthcare REITs like Ventas are expensive today, there are still plenty of others poised to profit from the retirement of the baby boomers—the strongest demographic shift in US history.

You just have to look where other investors don’t: in the mid-cap REIT space. Right now, I’m recommending three bargains with much fatter yields than Ventas … I’m talking payouts of 6.7%, 7.5% and 7.7%!

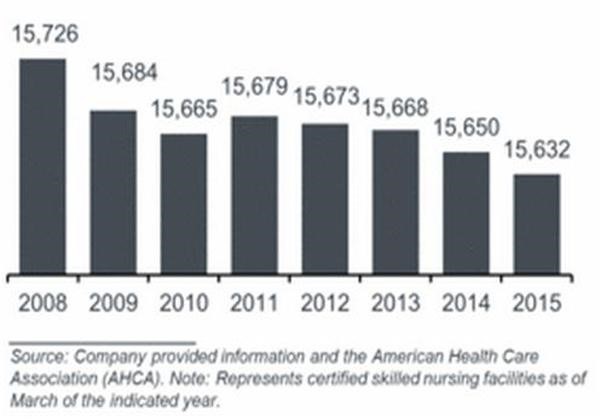

Two of these companies operate skilled nursing facilities (SNFs), the highest level of care a person can receive while still living independently. Here’s something few investors know: even though SNF demand is soaring, we actually have fewer of these facilities than we did in 2009!

Rising demand and falling supply will send these REITs’ cash flows soaring, driving a rising tide of dividend payouts for investors like you. I expect you’ll be raking in 10%+ on your initial investment in short order.

I’m ready to give you the names of all 3 of these top-quality income generators right now. Simply go here to discover them for yourself.