Preferred stocks are a little-known dividend secret. Worth knowing, by the way—they can yield up to 9.9%!

These “forgotten cousins” of common stocks can make a dividend portfolio. Plus, the discounts! Today we can buy a basket with some ingredients fetching as little as 89 cents on the dollar.

A quick refresher on preferreds. When a company needs capital, it typically either sells common stock—the AAPL to our Apple, the JPM to our JPMorgan—or bonds. But there is a third option, and plenty of companies use it: preferred stock.

Like common stock, preferreds give you a sliver of ownership in a company, they can improve in price based on the company’s performance, and they pay dividends. Unlike common stock, preferreds typically don’t enjoy voting rights, the dividend is usually fixed, and it trades around a par value. In fact, these are all bond-like traits, which is why preferreds are often referred to as “hybrids.”

But what really makes preferreds stand out is just how big those dividends are. A company’s preferreds will routinely pay in the mid- to high single digits, which will typically be 2x to 3x what they’re paying on their common shares.

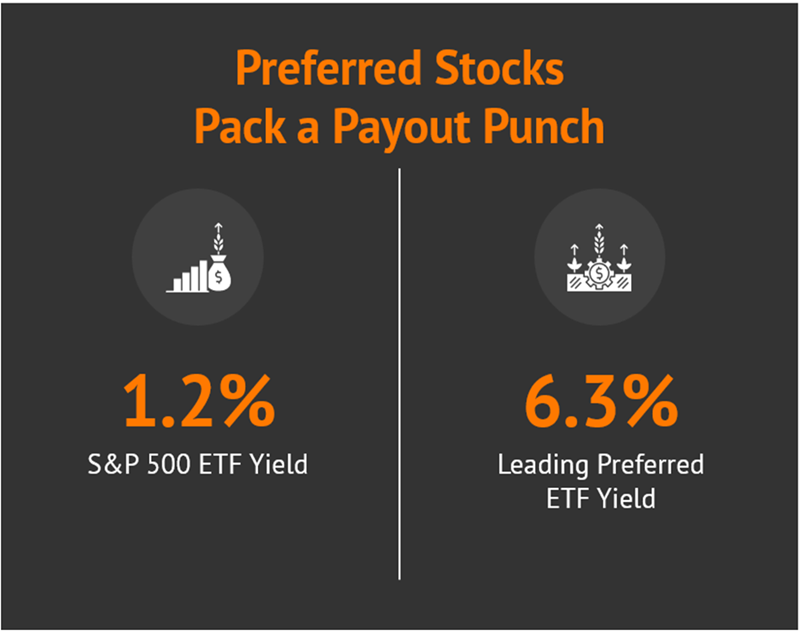

Just look at what a basic preferred exchange-traded fund (ETF) pays compared to the broader market.

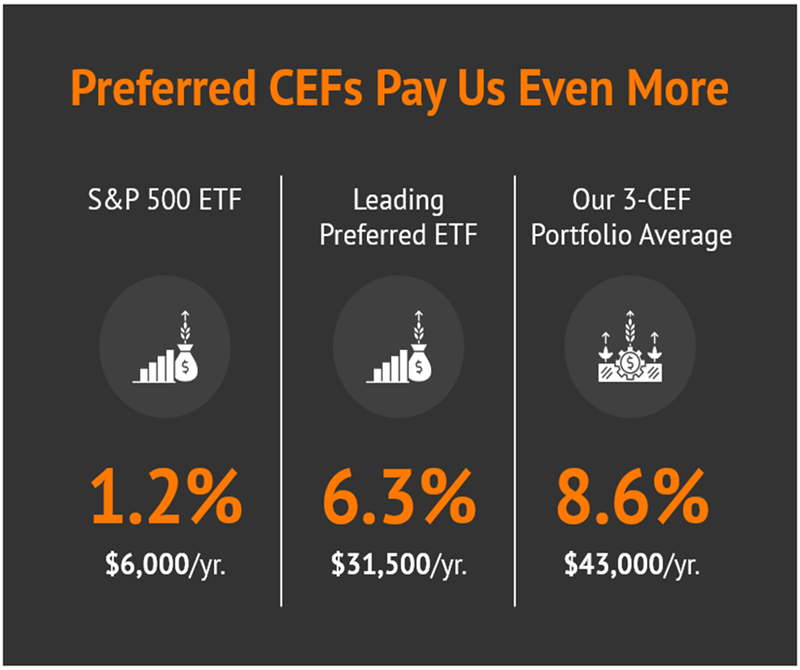

Funds in general are a great way to own preferreds for numerous reasons, not the least of which is that they often pay us monthly. But plain-vanilla ETFs have their limitations. They gobble up preferreds with almost no regard to quality or value, which is why we can often do better with human managers at the helm.

We could get that actively managed coverage through mutual funds, but closed-end funds (CEFs) are the superior play. Here’s why:

- CEFs’ prices frequently disconnect with the value of their assets, sometimes allowing us to buy a fund for much less than it’s actually worth.

- CEFs can take on debt to plow additional assets into their highest-conviction picks, which can supercharge performance and the yields they pay.

- CEFs can use options strategies such as selling covered calls to generate even more income than the portfolio would produce on its own.

The result? Yields that blow ETFs and mutual funds out of the water—and translate into a massive yearly salary of $43,000 if we put a $500,000 nest egg into the trio of CEFs I’m about to highlight.

And unlike preferred ETFs, we can buy these 7.6%- to 9.9%- yielding closed-end funds for discounts of between 4% and 11%.

John Hancock Premium Dividend Fund (PDT)

Distribution Rate: 7.6%

A great example of the difference the CEF structure makes is the John Hancock Premium Dividend Fund (PDT). Its 7%-plus yield would make it one of the top payers in ETF land, but it’s actually one of the lowest-yielding preferred closed-end funds … because management is playing with a little bit of a handicap.

PDT is a hybrid fund, investing roughly 50% of its assets in preferreds, and the other 50% in plain old common dividend stocks.

The preferred sleeve of the portfolio can hold its own. Its top holdings include preferreds from the likes of Citizens Financial (CFG), Wells Fargo (WFC), and Citigroup (C) that mostly pay in the 6%-7.5% range. The common sleeve? Sure, it includes Verizon (VZ) and a couple of other formidable dividend payers, but most of these companies are throwing off sub-4% distributions.

How does PDT bridge the funding gap? By throwing a lot of extra capital at management’s picks—the fund’s debt leverage currently stands at a thick 34%.

Over the very long term, this willingness to bet big has made itself apparent in two ways:

- Much more volatility than a basic portfolio of preferreds.

- Returns that not only blow vanilla preferred ETFs out of the water, but are also mighty competitive with even 100% dividend-equity funds.

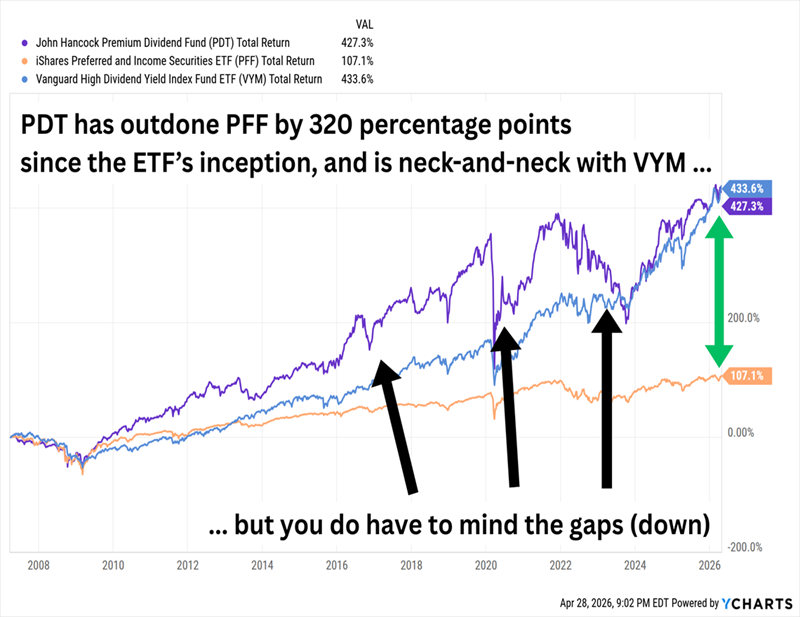

This Hybrid Portfolio Has a Lot of Horsepower

Despite its run of late, John Hancock Premium Dividend Fund is trading at a wide 11% discount to its net asset value (NAV), meaning we’re effectively buying its preferreds for 89 cents on the dollar. That’s not just cheap on its face—it’s a relative bargain for this monthly payer, too. PDT has, on average, traded almost in line with its NAV over the past five years.

Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund (PTA)

Distribution Rate: 8.3%

Most of us have been trained to see “tax-advantaged” and think “municipal bonds.”

As much as I’d like to give Uncle Sam the slip on my preferred payouts, that’s not quite what the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund (PTA) has to offer. Instead, PTA aims to minimize federal income tax consequences on its dividends by owning preferred stocks that pay qualified dividends—which are taxed at the more favorable long-term capital gains rates—and by adopting more of a buy-and-hold mentality so as not to trigger short-term capital gains. (And when it does pick up short-term capital gains, it’s mindful about offsetting those gains with short-term losses.)

Management isn’t exactly breaking its back to do this. Most preferred stocks pay qualified dividends. And preferreds aren’t exactly day trading fodder, either.

This is a global portfolio of about 300 preferreds, split roughly 50/50 between the U.S. and the rest of the world, mostly developed Europe. Financials, like BNP Paribas (BNPQY) and Royal Bank of Canada (RY), are dominant at almost 75% of assets, which is par for the preferred course. Credit quality is fine if not a little low; about 55% of assets are allocated to investment-grade preferred stocks. Leverage is even higher than PDT, at 35%, helping juice the payout above 8%.

PTA has only been around since 2020 and didn’t exactly charge out of the gate. But a lot of that had to do with timing—many preferred funds took it on the chin through the rate hikes of 2022 and 2023.

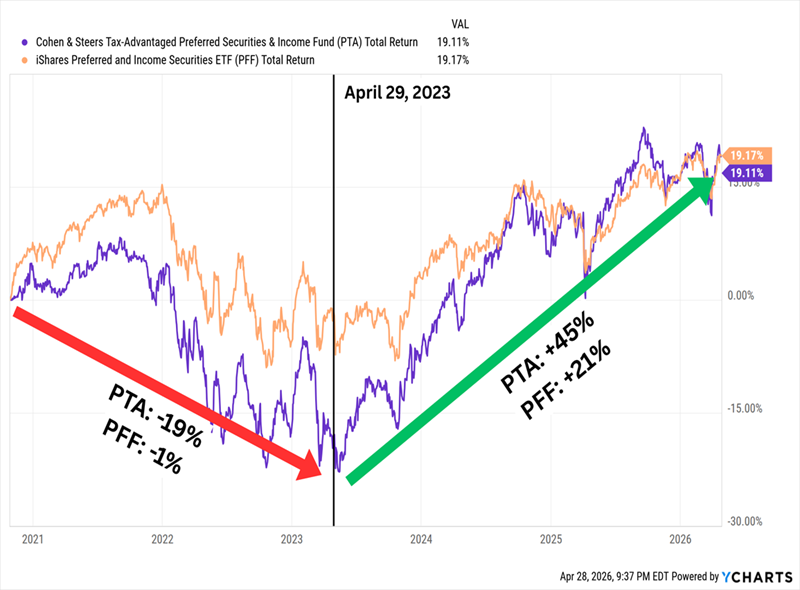

Since Its 2023 Bottom, PTA Has More Than Doubled Up the Preferred Standard

Cohen & Steers’ fund is trading at a 7% discount that looks decent in a bubble. However, its five-year average discount is only a hair lower, so it’s technically less expensive than normal, but it’s not a screaming deal.

We can’t get too attached, though. Like with some other CEFs, PTA is a “term” fund that’s scheduled to liquidate on Oct. 27, 2032, though the fund’s board of trustees technically could vote to extend its life by up to two years.

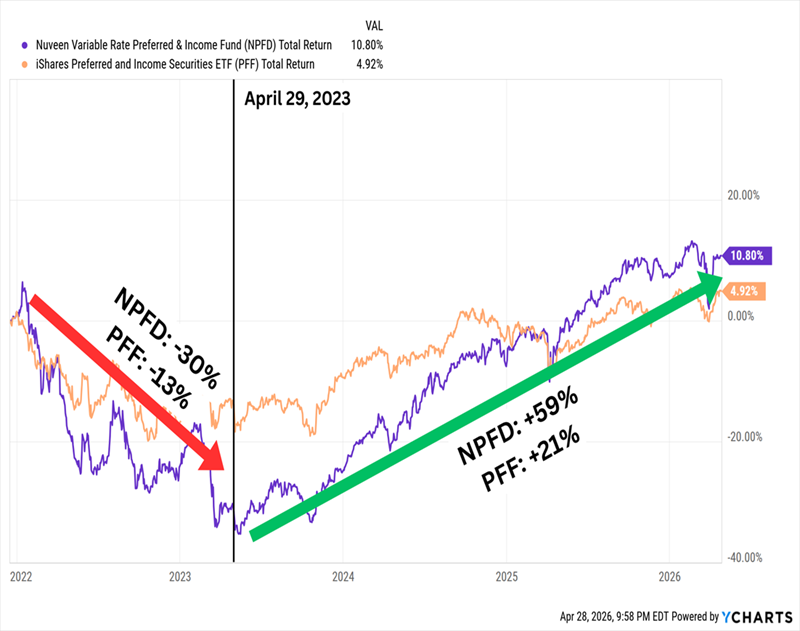

Nuveen Variable Rate Pref & Inc Fund (NPFD)

Distribution Rate: 9.9%

The Nuveen Variable Rate Preferred & Income Fund (NPFD), which came to life in 2021, has a similar story. It started trading not long before the Fed’s tightening pounded preferreds, so it looked awful from the start—but it has been in a relative sprint ever since bottoming out in 2023.

Preferred stocks usually pay a fixed dividend, but as this Nuveen fund’s name implies, NPFD is interested in variable-rate preferreds. Sort of.

Most of NPFD’s assets (about 85% right now) are invested in “fixed-to-fixed rate securities,” which step from one rate to another based on a set schedule, not underlying interest rates. Another 9% is dedicated to fixed-to-floating rate securities, which start with a fixed coupon that it pays for a few years before switching to a variable-rate coupon. It even holds a few fixed-rate securities. In all, only about 5% of assets are invested in truly variable-rate preferreds.

The rest of the portfolio details are pretty standard. This is another global preferred fund, at a roughly 60/40 U.S./international blend. About 75% of assets are in investment-grade preferred, so credit quality is good. And the 185-stock portfolio is amplified with 26% debt leverage.

Income investors would be hard-pressed to find a better preferred yield than what NPFD offers—at last check, it was the highest-yielding preferred fund on the market.

A discount to NAV of 4% is modest in the first place, but it’s actually more expensive than its long-term average discounts of almost 9%. So we’re not getting a screaming bargain here—but nearly 10% a month, paid monthly, papers over a lot of sins.

How to Secure Steady Monthly Dividends of Up to 14.9%

If your experience is anything like mine, you’ve been watching your monthly bills climb higher and higher for years—and fast.

Inflation is eating away at Americans’ financial security, which is why people closing in on their nest-egg targets for retirement are suddenly starting to get the jitters.

$1 million to comfortably retire? Yeah, maybe before COVID.

But here’s the thing: You very well may be able to clock out on a realistic amount of money—much less than a million, in fact.

You just can’t do it holding Dow Jones blue chips.

You need true dividend powerhouses—like the companies I prioritize in my “9% Monthly Payer Portfolio.”

It’s all in the name. These generous stocks and funds average a yield of more than 9% across the board, and some of them pay up to almost 15% a year. That’s enough to live on dividends alone without ever needing to break off a piece of your nest egg to generate cash.

So, retirement on less than a million dollars? Yes. Here’s the math:

- A $600,000 nest egg could earn $54,000—in many places in the U.S., that’s enough for a fully paid retirement without even factoring in Social Security!

- And let’s say you have managed to stash away a cool million bucks? The 9% Monthly Payer Portfolio would pay you a downright lush $90,000 in dividend income every year.

And you’re not cashing these dividend checks annually. Not quarterly, either.

You’re cashing them every single month.

No dumping money into certain stocks because you’re getting underpaid every third month—just paydays as smooth as when you were collecting a paycheck!

These monthly payers won’t stay this cheap for long. Click here for all the details, and turn your portfolio into a monthly dividend machine!