Right now, thousands of Americans are making a mistake that threatens to lock in the losses they’ve suffered in this downturn.

Worse, these folks will be stuck on the sidelines in the rebound, watching helplessly as other stocks soar and their holdings stagnate, or even drop further.

I’m talking about people who hold master limited partnerships (MLPs) and buy into the myth that these companies—owners of oil and gas pipelines and storage facilities—are simply “toll bridges,” making them a relatively safe play on energy.

Worse, many of these folks think MLPs can benefit from the huge glut of oil and gas building up around the globe. Throw in these companies’ huge 8%+ yields and, to these investors, anyway, MLPs seem like a can’t-lose proposition.

Unfortunately, this line of thinking is outdated—and dangerous. The truth is, you’re better off looking outside energy altogether for income, namely to a diversified set of high-yield closed-end funds (CEFs). (I’ll give you access to my 4 favorites—throwing off high, steady dividends of 8.4% and up—at the end of this article.)

Here are three reasons why you need to stay well clear of MLPs now, and dump any you already own immediately.

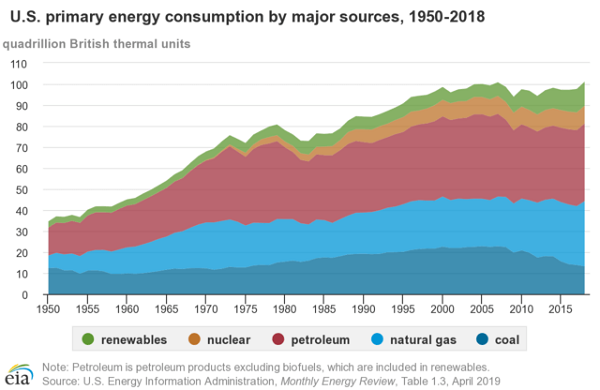

MLP Danger Sign No. 1: Oil Use Is Plunging

Even before Covid-19, oil was being hit by two big trends: more efficient machines and a shift to alternative energy.

Above, you can see that petroleum and natural gas consumption (in red and light blue) fell from its peak in the mid-2000s and never recovered. That drop was partly started by the Great Recession, then the growth of renewables (in green) and more efficient appliances kicked in.

With energy-sipping appliances, cars, planes and heating systems, the world has needed to burn less oil and natural gas to get the same output. This means that even if oil demand rises, it won’t climb by much. And it will likely go down in the post–Covid 19 world as more people work from home and look for other ways to cut energy use.

MLP Danger Sign No. 2: MLPs Are Tied to Oil (Just Not the Way Most People Think)

Slack demand caused oil prices to crash twice in the last decade: in 2014 and in 2020. When oil tumbled this year, even one of the largest and presumably safest MLP wasn’t immune. Enterprise Products Partners (EPD) fell alongside the Alerian MLP ETF (AMLP):

MLPs Crash

And MLPs are one place where waiting out the crash and/or buying the dip aren’t prudent strategies. Just ask investors who’ve held MLPs since the 2014 oil-price collapse—they’re still waiting to get their money back.

MLPs Down for the Count

The question then becomes: if MLPs don’t produce oil—they just store and ship it, remember—why are their shares dropping with oil prices? Their services are still required, and cheaper oil should translate into more demand, so more oil will be stored and transported, right?

While that makes intuitive sense, energy markets are rarely intuitive. The fact is, MLPs depend on oil producers for their revenue; if producers can’t afford oil transport, or if the producer goes out of business, the MLP loses sales. That means MLPs can’t pay their debts, meaning dividend cuts are sure to follow. They’re already happening.

MLP Danger Sign No. 3: Oil Prices Can Go Lower

The lower oil prices go, the bigger the risk that MLPs will see their oil-dependent revenue fall. But how low can oil prices go?

They could actually go to zero—and even below. Crude from the Canadian oil sands, for example, has been trading in single digits lately. And in late March, Bloomberg reported that a grade of crude called Wyoming Asphalt Sour, which is mainly used in paving, received at least one negative bid. In other words, the buyer was asking the seller to pay them to take the oil away!

Let’s for the sake of speculation say we found ourselves in a situation where more crude was selling for negative prices. Wouldn’t that still benefit MLPs, as they would still be providing shipping services? It’s true that this could be a profitable business, but not with MLPs’ current cost structure and debt load. If such a scenario came to pass, many MLPs could go bankrupt, leaving shareholders holding the bag.

Before I sign off, let me give you a final reason to steer clear of MLPs, especially if you buy them individually and not through a CEF or other type of fund: they issue a K-1 package at the end of the year, instead of the neat 1099 form. We don’t need to get into the weeds; suffice it to say, K-1s are a headache for the person who does your taxes (whether it’s you or a professional.)

These 8.4% “Dividend Lifeboats” Are Perfect Buys Now

Despite the fear-laden headlines, now is the time to be buying, not selling. But with the wild volatility we’re seeing, we do have to be extra careful about what we add to our portfolio.

As I just explained, this is not the time to buy MLPs (and that time may never come!). Even the typical S&P 500 name is a dangerous proposition, for a reason you might not expect: these stocks’ lame dividend payouts—a pathetic 2.2% yield, on average, even after the selloff!

If we really want to protect our retirement (and grow our income stream), we need to demand way more of our return in safe cash.

How much more? I’m talking dividend payouts of 8% and up. That could be enough for you to live on dividends alone and do what every investor would love to do right now: turn off the daily market gyrations and enjoy a serene life of steady dividend checks.

Because if your income stream is safe—and big enough to fund your lifestyle—there’s absolutely no need to watch stock prices like a hawk.

I’ve uncovered 4 funds that can make this seemingly impossible dream a reality. They yield 8.4% today, and that’s just the average—one of these funds throws off an outsized 10.3% dividend now. Put, say, $150K into this steady high-yielder and you’re looking at a steady $15,450 coming back your way every year.

Don’t listen to the pundits who say you can’t find high, safe dividends in this crisis. Build your income stream (and your nest egg) with the 4 funds I’ll share with you now. Click here and I’ll give you all the details on these 4 stout 8.4% payers: names, tickers, complete dividend histories and everything else you need to know before you buy.