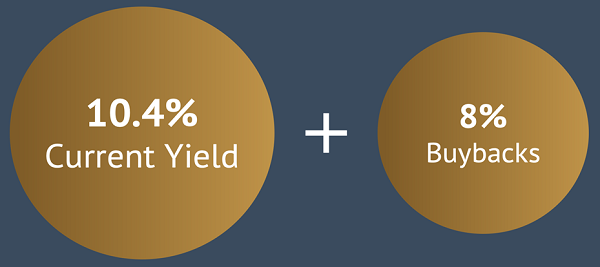

This dividend stock yields 10.4%. But really it boasts an annual “hidden yield” of 18.4% when we consider buybacks.

Eighteen-point four percent per year. Wait, what?!

(Your strategist pauses to point upwards towards the late, great Norm Macdonald.)

A Hidden Yield Formula for 18.4% Yearly Returns

Now what if I told you this stock was also being heavily shorted? Over 11% of this company’s outstanding shares are being sold short. This is fuel for a potential rally because these positions must be bought back later.

Remember, when traders sell a stock short, they book the sale in advance. “I think this stock is so terrible, I want to sell it at today’s price.”

They’re selling it before they buy it. Their bet is that the price will fall. “I’ll buy it back later at a lower price,” closing the short position and profiting on the difference (minus the cost of the margin loan and any dividends, which the short seller must pay).

These bets become especially tricky when everyone’s doing them. We recall what happened with GameStop (GME):

- Hedge funds were massively short GME (more than 100% of its shares were sold short!).

- Internet bros and gals learned this and started buying.

- Hedge fund Melvin Capital joined in, got squeeeeeeeeezed and imploded entirely.

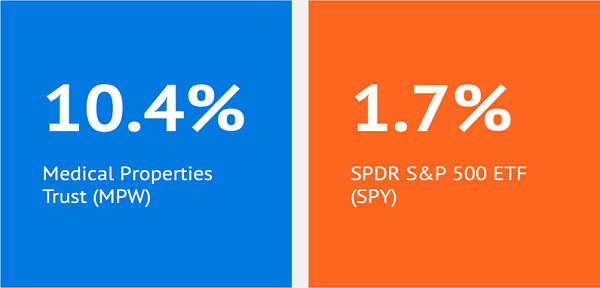

Compared with GME, the 11% short position in Medical Properties Trust (MPW) is modest. But this is a 10.4% payer. Shorting a dividend stock is the ultimate sign of disrespect because the short seller is on the hook to make the dividend payment.

I don’t know about you, but when I’m investing, I prefer not to have a 10.4% tab at the stock bar running against me.

Yield Comparison (It’s No Contest)

MPW is not a fly-by-night company, either. It does not have an aging business model like GME. The firm actually benefits from the aging of America!

Years ago, easy financing didn’t exist for hospitals. If someone wanted to build a hospital, their only option was a traditional corporate loan package. This was a big headache because it forced the hospital to lock up all of its asset value as collateral.

Ed Aldag founded MPW in 2002 to tackle this problem. He and his team developed low-cost and flexible alternative financing for hospitals. It worked! Ed’s company is the largest investor in hospital real estate in the U.S. today.

Largest “investor” is crucial: MPW doesn’t run hospitals, it invests in them. The company provides capital to the operators, particularly proven ones. In turn, they use the money to improve their facilities, upgrade their technology, hire more staff, and expand their complex (and pay back their loans).

Yet, holding MPW can be quite the rodeo. You wouldn’t expect this from a steady dividend payer (and dividend grower!), but headline news can rattle this stock. The hospital operators may provide reason to worry.

Back in 2017, MPW plunged on worries that hospital operator Adeptus Health was in trouble. Investors feared missed or reduced rent payments. Their concerns were valid—it declared bankruptcy in 2021—but the problems never spilled over into MPW. We held the stock and actually “doubled down” during the Adeptus scare because we realized the contagion fears were overblown.

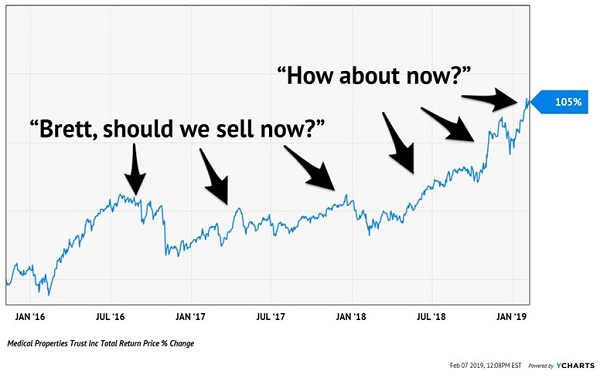

The first time we held MPW in our Contrarian Income Report portfolio, we scored 105% total returns, including $3.09 per share in dividends. That was good for a 28% cash return on our initial $11.13 purchase. With MPW humming through the worries there was no reason to cash in too early. We waited until March 2019 to sell to book gains:

MPW Rewarded Patience: Nov ’15 through Mar ‘19

Our second go-round with MPW hasn’t been so kind. But it may now be at an inflection point.

Last week, its Board of Directors announced a $500 million repurchase authorization. This gives Ed and his team the OK to buy back a whopping 8% of the company’s outstanding float in the next 12 months.

When a stock is this cheap, a buyback can really ignite the price. Personally, I love this move. It’s annoying when managers complain about their stock being too low, or short sellers ruining their lives.

Buy back your cheap shares. Put your money where your mouth is.

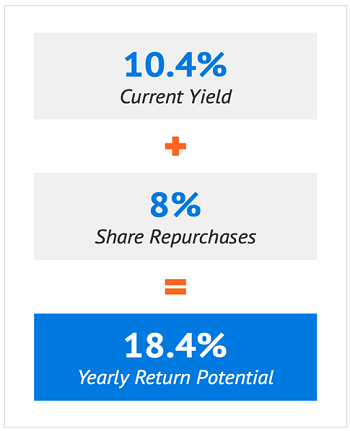

This gives Ed and his team the compelling 18.4% total return outlook I mentioned earlier. We have a 10.4% cash yield (paid quarterly at $0.29 per share) plus 8% of the shares being repurchased.

This buyback should make every metric look better on a per share basis. It will also support and even boost the dividend, because of all the cash conserved when 8% fewer shares need a payout!

Remember, this is an annual saving for MPW. It’s more future money that management can use to buy back even more shares, raise its payout or invest in acquisitions that will further grow cash flow.

The return on investment from this buyback is outstanding. It starts at 18.4% and really, it will be an even higher ROI thanks to the “virtuous cash cycle” the repurchase is kicking off.

MPW shorts are officially on notice. Watch out bears, because these shares are ready to squeeze higher quickly!

This is the “15% returns every year” formula that I love. Bull or bear, I really don’t care—just give me a dividend, future payout hikes plus some share repurchases and we’ll grind our way to a fabulously steady 15% or better. Here’s how.