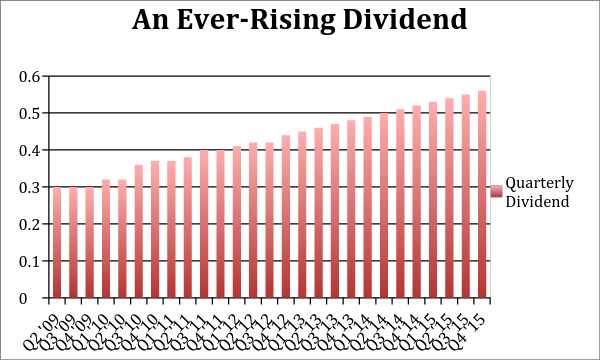

Stocks that raise their dividend meaningfully every year will make you a lot of money over the long haul… provided they continue to boost their payouts, of course.

Studies by two global investment heavyweights, BlackRock and GMO, have shown that 90% of U.S. equity returns over the past 100 years have been thanks to dividends and dividend growth.

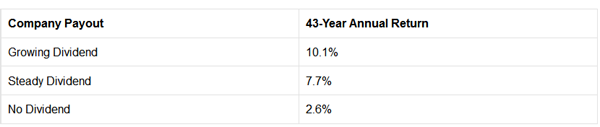

Ned Davis Research also conducted its own 43-year study on stock returns (from January 1972 through December 2014). The conclusion? Dividend payers are good… but dividend growers are great. Stocks that paid a growing dividend delivered double-digit returns and outpaced steady dividend payers by nearly one-third:

Annual Rate of Return (Ned Davis Research)

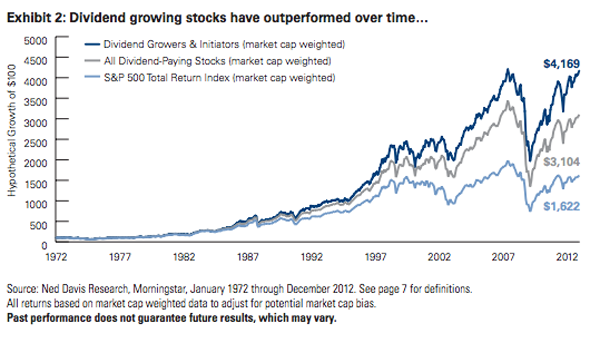

Over time, this compounding really adds up as these stocks pull away from stagnant payers and the market at-large:

Dividend Growers Pull Away Over Time

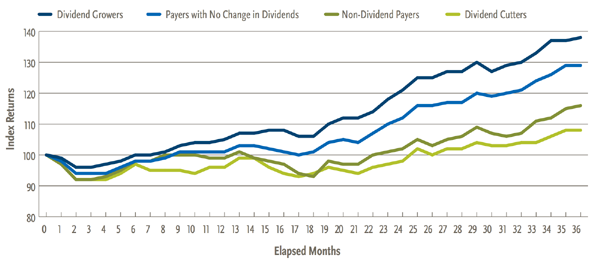

Worried about the Fed’s rate cycle? Research from investment firm Nuveen shows that dividend growers outperform their counterparts for the 36 months after a Fed rate increase as well.

Dividend Growers Win the 3 Year-Period After Rate Increase, Too

Companies with profits that grow year-after-year are able to share these rewards with their investors. Dividend growth is the sign of a healthy, thriving business with a sustainable “unfair advantage” over its competitors.

Most dividend aristocrats – companies that have raised their dividends for each of the last 25 years – have enjoyed earnings that have risen in tandem with their payouts to shareholders. And while some have timeless business models that will continue to power payouts for years and decades to come, others are hitting a wall when it comes to earnings growth.

It’s important to buy the aristocrats of tomorrow, rather than fixating on the payout heroics of yesterday. Let’s start with 3 businesses that continue to roll with the world’s changes…

3 Dividends That’ll Keep Growing For Decades

Hormel Foods (HRL) has returned a cool 498% to investors over the past 10 years. The company boosted its dividend by 314% over the same time period.

Hormel Investors Chow Down on Dividends and Gains

The specialty food maker owns more than 30 brands with #1 or #2 market share positions in their respective category. Hormel has beaten analyst earnings estimates for each of the last four quarters, and compounded its free cash flow (FCF) by 21% annually since 2011.

Management projects 14-18% earnings-per-share (EPS) growth in 2016. Its brands (like Applegate meats and Muscle Milk) are well aligned with current consumer tastes… unlike another food company we’ll be discussing shortly.

Steel producer Nucor (NUE) has bumped its dividend every year since 1973. It’s not really a stock to sock away forever, given the cyclical nature of steel prices. But it’s a very well-run company that makes money in good times and bad, and its financial consistency is quite impressive given how volatile steel is.

And with steel at its lowest levels since the Great Recession, this is the time to make a contrarian play on Nucor. It has 20% upside from here if the global economy stays on track – and you’ll collect its 3.8% dividend while you wait.

Finally AT&T (T) is gaining momentum thanks to its DIRECTV acquisition. It’s returned 10.2% to investors, including dividends, since the deal closed – versus a negative 7.6% return for the S&P 500:

AT&T Investors Enjoy Their Satellite Entertainment

Free cash flow (FCF), which had been declining since early 2013, is up 63% on a TTM (trailing twelve month) basis. The stock pays 5.2% today, and should continue to benefit from its new satellite entertainment.

And 3 Washed Up Dividend Aristocrats To Sell Now

Not all dividend-paying legends are cut out for the year 2016. Here are three washed up payout princes I’m particularly concerned about…

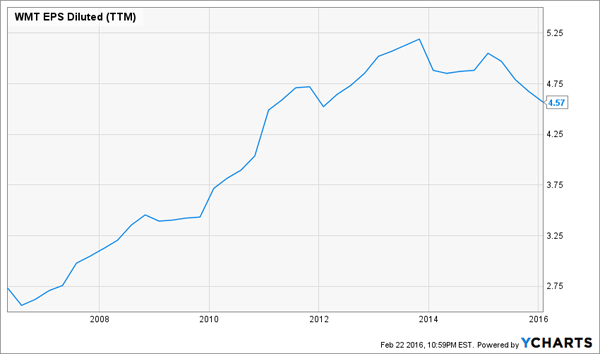

Wal-Mart (WMT) tripled its dividend since 2005 – mostly because it was able to double its payout ratio over the same time period. Problem is, going forward, there’s not much room to boost from here:

No More Easy Payout Increases

The retailer really needs to reinvest earnings in new stores and new technology. Amazon.com (AMZN) continues to rake in sales online that would’ve been making in-person at Wal-Mart just a few years ago.

Wal-Mart isn’t going to be able to beat Amazon online, which means its earnings are going to continue to stagnate. So will its stock price.

Wal-Mart Earnings Hit a Wall

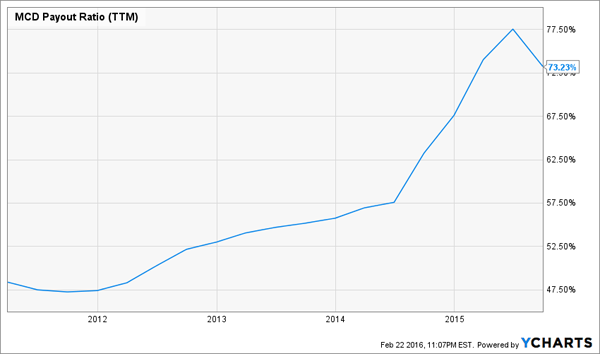

Speaking of earnings walls, let’s talk about McDonald’s (MCD), which – despite the recent favorable press – is still on the wrong side of every food trend in America. Earnings-per-share (EPS) are flat over the last five years, while dividends are up 46% over the same time period.

Where’s this magical payout growth coming from? The payout ratio, of course, which has ballooned to 73% of earnings:

Ronald Needs a Second Job… To Pay the Dividend

Ronald McDonald may need to start flipping his company’s valuable real estate in addition to burgers to satisfy the company’s dividend-hungry investors. Mickey D’s also sports a price-to-earnings (P/E) ratio of 24, higher than its 20-year average of 19. Investors are paying more today, for much less growth, which doesn’t make a lot of sense.

While Wal-Mart and McDonald’s just fell behind the changing times, healthcare REIT HCP (HCP) has everything going for it and just can’t execute. There are 77 million baby boomers just starting to retire now, yet HCP can’t figure out how to make money on its skilled nursing facilities:

This problem is unique to HCP, because the biggest demographic shift in American history is in healthcare’s favor. Consider that…

- Roughly 10,000 baby boomers will turn 65 every single day for the next 17 years

- We’re living longer than ever… but we’ll require more care as we get older

- Healthcare spending in the U.S. will increase to $5.43 trillion by 2024

If you own HCP, I’d trade in the laggard for the top company in its sector. This firm pays a gaudy 7.5% dividend today, and it actually increases its payout not just every year, but every single quarter:

AND this company just reported great earnings right after HCP’s disappointment. It’s on sale thanks to HCP’s incompetence, and if you buy this stock today, you’ll see a 10%+ annual yield on your initial capital in no time at all.

Remember, that dividend will increase every 3 months – which is why I’m telling my subscribers to lock in this growing income stream today, while it’s so cheap. Get the details on this future aristocrat (along with my two other favorite 8% payers) and start compounding your wealth right now.