Real estate investment trusts (REITs) are on fire—and we need to be very careful not to get burned.

Yellow Light on Some (but not all) REITs

Look above and you’ll see what I mean—the Vanguard Real Estate ETF (VNQ), in blue, has topped the S&P 500 on price returns alone. That’s a monster run for income investments like REITs.

More REIT Gains to Come—But Be Cautious

Here’s the twist: there’s plenty more upside ahead—and you can thank the Fed for that. Its latest rate cuts will keep powering REITs higher, for two reasons:

- Lower rates cut REITs’ borrowing costs, and these trusts (owners of everything from senior-care centers to cell towers) need lots of borrowed cash to buy new buildings and upgrade current ones.

- Savers are getting clobbered: With 10-year Treasury rates at 1.8%, REIT dividends, which can run into the 7% range, look very appealing by comparison.

And what if we see negative interest rates in the US? It’s something everyone from former Fed chair Alan Greenspan to the head of fixed income at JPMorgan Chase (JPM) says could very well appear.

What would happen to REITs then?

Their 2019 spike would be a puff of smoke compared to the surge we’d see. Because almost any yield (let alone a growing 5%+ payout) would be irresistible compared to putting your cash in a Treasury note and getting less than your principal back!

But we can’t just grab the REITs with the biggest dividends and call it a day. Because this latest run has already pushed some REITs to valuations far out of whack with their fundamentals.

If we buy these “dividend land mines,” we could lose 10%, 20% or even 30% of our capital! It’s the same risk as buying a regular stock at a high price-to-earnings ratio.

So how do we tell when a REIT is overpriced? Its share-price movements are only half the story, because a big move up could be warranted if the REIT has the rising cash flow to back it up.

How We “Timed” This Cheap 7% Dividend for 24% Upside

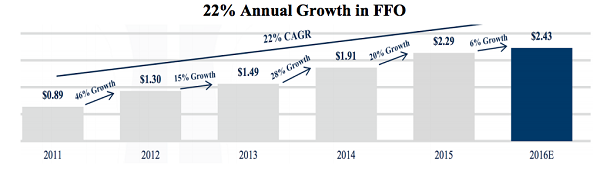

Which brings me to hotel operator Chatham Lodging Trust (CLDT), which I recommended to my Contrarian Income Report readers in December 2016. It’s a great example of how you can use a critical REIT metric—funds from operations (FFO)—to separate bargains from overpriced REITs.

(My new “REIT playbook” gives you my proven 5-point strategy for grabbing big dividends, and upside, from bargain-priced REITs. Discover it for yourself, free, right here.)

When I recommended Chatham a little less than three years ago, it traded at a bargain 8.4-times FFO.

Why so cheap? Investors fretted that Airbnb would swamp Chatham’s hotels. But that ignored the fact that most of its locations are near airports or in suburbs, far from Airbnb’s downtown turf. When you looked “under the hood,” things got better:

Source: Chatham Lodging Trust

That outsized 22% average yearly FFO growth was driving a surging dividend, up 57% in just three years! Best of all, this stock yielded 6.8%—its highest level ever.

What happened after our buy call? Chatham soared, handing us a market-crushing 24% total return in less than two years.

But by September 2018, Chatham’s price-to-FFO ratio got a little too plump, at 10.7-times. The cat was clearly out of the bag, so we checked out. Here’s what happened to Chatham next:

We Sidestepped a 16% Dive

Now let’s look at three REITs investors are blindly piling into, overinflating their valuations and setting them up for Chatham-like plunges of 16% or more.

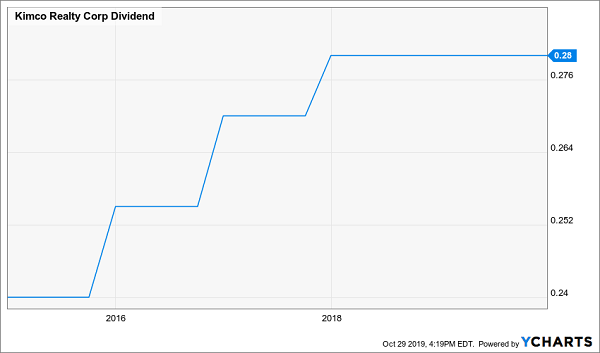

Overpriced REIT No. 1: Kimco Realty (KIM)

Kimco Realty just might tempt you with its 5.2% dividend, but don’t take the bait. First-level investors have bid the mall landlord’s stock into the stratosphere, up a whopping 48% year to date, far ahead of VNQ:

Kimco Buyers Get Ahead of Themselves

A chart like this might be okay if Kimco’s FFO had kept pace with its rising share price. But FFO was up just 3.4% in the third quarter.

That, along with the soaring share price, means you’ll pay 15-times adjusted per-share FFO today, compared to 9.7-times a year ago. Worse, dividend growth has stalled:

Frozen Dividend an Early Warning

A soaring valuation and a frozen dividend are a classic setup for a correction. And that’s before we even talk about the challenge mall operators like Kimco face from Amazon.com (AMZN). Stay away.

Overpriced REIT No. 2: Independence Realty Trust (IRT)

Apartment landlord Independence is another REIT that’s gotten ahead of itself, with a share price that’s spiked 67% from January 1, nearly tripling VNQ’s gain.

Another REIT in Too Much of a Hurry

Sure, Independence is performing pretty well: core FFO rose 3% in the third quarter, and average rental rates gained 5.7% across its portfolio. The stock also yields a tidy 4.7%—though the payout does consume a tight 95% of per-share FFO, so there’s little potential for a raise.

The main problem is that shares now trade at 20.4-times core FFO, compared to 12.3-times a year ago. That’s far too high for an apartment landlord, and it sets the stock up for a hard fall on any bad news.

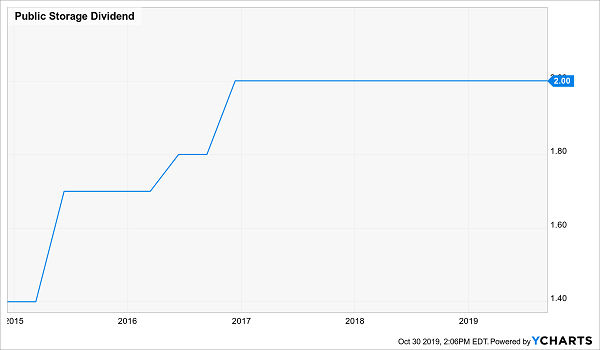

Overpriced REIT No. 3: Public Storage (PSA):

We need to talk about Public Storage, the biggest self-storage player, with 2,500 facilities. The company yields 3.6% now, and it’s been left behind in the REIT run, with just a 9% gain year to date.

So is PSA a bargain—or does it have further to fall?

The latter. Here’s why.

For one, even after the stock plunged on disappointing third-quarter results last week, PSA still trades at 20.5-times FFO. That’s out of whack with a company whose core FFO barely budged, up just 1.1% from a year ago.

Worse, the cost of running its business jumped 6.4%, including a whopping 69.5% increase in marketing costs, as Public Storage spent heavily to attract new clients in the highly competitive (and fragmented) self-storage market.

With costs rising, dividend growth has taken a back seat: the payout hasn’t budged since PSA rolled out its last hike nearly three years ago.

PSA’s Payout: On Ice

The bottom line? I don’t see any point messing around with a pricey REIT with a stalled dividend when there are plenty of trusts with higher yields and growing payouts to choose from.

Prediction: My 2 Top REITs Will Soar 25% in 2020 (and yield 7%+)

Case in point: the 2 cash-rich REITs I urge you to add to your portfolio now.

Why am I so adamant about them?

Because both of these fresh 7%+ yielders are ridiculously cheap. That, plus the “fuel” from the Fed’s latest rate cuts, brings me to one inescapable conclusion:

Both of these REITs are “spring loaded” for 25% price upside in 2020!

The best part? While you wait for that upside to kick in, you’ll pocket their huge cash dividends: I’m talking 7% and 8.9% yields here.

The names of both of these blockbuster REITs are waiting for you here. The time to buy them is now, before the latest rate cuts start pushing their share prices higher.

And that’s not all.

I also want to show you my entire REIT-picking strategy at no cost whatsoever. This simple 5-step plan steers you around overpriced pretenders and toward the safe 7%+ dividends you need for retirement.

The whole system—the same one that’s delivered a steady 11.7% average annual return (with most of that in dividend cash) to members of my Contrarian Income Report service—is one click away.

Don’t miss out. Go here to discover my 2 very best picks in high-yield REITs now, plus get instant access to my complete 5-step REIT-picking system.