Today I’m going to reveal my personal strategy for outperforming the market over the long haul.

It’s simple. All you have to do is buy dividend stocks—but not in the way most people think.

I’ll also name 4 terrific dividend growers you can buy now and safely tuck away in your retirement portfolio forever. More on those in a moment. First, we need to talk about…

The Wrong Way to Buy Dividend Stocks

When picking stocks for the long haul, many folks put too much emphasis on the current dividend yield.

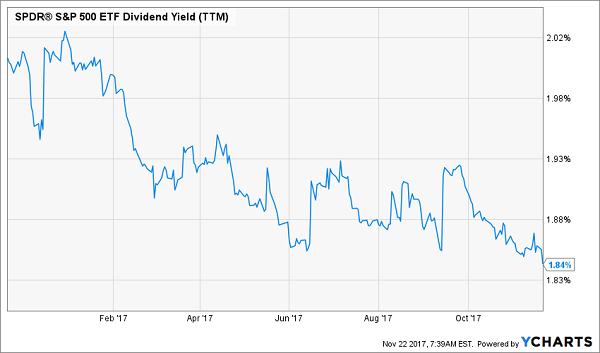

Trouble is, the high yielders that could really make a difference to your retirement—I’m talking payouts of 6%, 8% and up—are getting scarce as the S&P 500 grinds upward:

Few Trophies for Dividend Hunters

Worse, a high yield can easily lead you onto the rocks, something many people learned the hard way with telecom operator Frontier Communications (FTR).

A year ago (and many times since), I warned that its 12.9% yield was a house of cards. One number explained why: the payout ratio, or the percentage of earnings paid out as dividends.

Back then, this ratio was negative, so management was paying the dividend while losing money!

When the inevitable cut came, the reaction was swift and brutal:

FTR’s Dividend Disaster

That sickening drop has left the stock with a ridiculous 33.9% yield today. And it’s an even bigger sucker’s bet now.

For one, the payout ratio is still negative, losses are widening, and FTR is carrying $17.6 billion in long-term debt. That’s almost 32 times its $555.5-million market cap (or the value of all of its outstanding shares)!

A Better Way to Buy Dividend Stocks

Traps like Frontier are why we need to look past current yields and hone in on stocks with strong dividend growth backed by rising earnings and cash flows.

And when we find these gems, we need to hang on with both hands!

This is the safest and most reliable way to get rich in stocks. Because the longer you hold a top-flight dividend grower, the higher the yield on your initial buy gets.

This ignored number is a retirement game changer—as the first buy-and-hold “forever stock” I want to show you demonstrates.

“Forever” Stock No. 1: Life Storage

Let’s say you invest $10,000 in Life Storage (LSI) a self-storage REIT I first flagged as a buy-and-hold “forever stock” on September 23. Right now, LSI yields 4.5%, so you’d get $450 in annual dividends.

That’s not bad!

But let’s say its payouts rise to $600 a year—a 33% increase. Then you’d be effectively earning 6% on your original $10,000. As the trend continues, you could easily end up earning 10% or even 20% a year just from rising dividends.

That’s easily attainable dividend growth for LSI, whose payout has more than doubled in the last five years.

There’s more on the way: revenue and funds from operations (FFO)—a key REIT metric—are both surging, and the $4 annual dividend is easily covered by the trust’s forecast 2017 FFO of $5.26 to $5.30.

Now let’s move on to 3 more stocks perfect for generating these life-changing “hidden yields.”

“Forever” Stock No. 2: Uncle Sam’s Landlord

Easterly Government Properties (DEA): If there’s one trend we can rely on, it’s that government will keep growing.

The good news? Easterly is in the sweet spot. The REIT rents its 46 properties to 20 US government agencies, including the Department of Veterans Affairs and the FBI.

This truly is one of the most boring businesses I’ve ever seen, but it’s delivering a steady rise in FFO. Management expects $1.26 to $1.29 a share for all of 2017, up smartly from $1.21 last year. And it’s pegging another nice bump for 2018, to between $1.31 and $1.35.

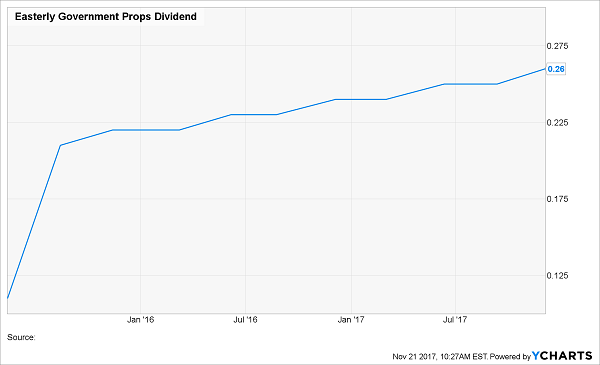

No wonder Easterly has the confidence to raise the dividend twice a year, as it’s been doing since its IPO in February 2015:

A Quiet Dividend Champion

The best part: the stock already yields 4.6%, so you’re not sacrificing current income to get that payout growth!

The trust also boasts another stat you rarely see: its portfolio is 100% occupied.

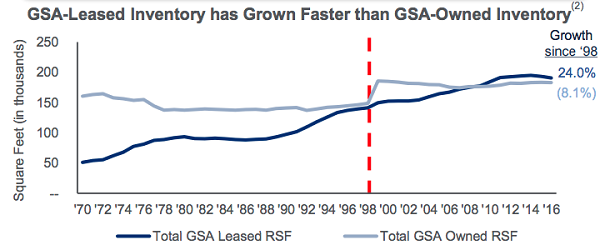

That’s because the bureaucrats adore its energy-efficient buildings (average age: 11.8 years), and the feds have long been moving from being owners to renters. That trend will only accelerate as budgets tighten:

Source: Easterly Government Properties November 2017 Investor Presentation

That, plus Easterly’s rising FFO, makes this dividend safe: the $1 of total payouts in the last 12 months is a very manageable (for a REIT) 78% of the midpoint of Easterly’s 2017 FFO forecast.

The kicker? Easterly is cheap at 16 times the midpoint of forecast 2018 FFO. So put this safe—and growing—payout on your shopping list now.

“Forever Stock” No. 3: A Fire Sale That Won’t Last

Prudential Financial (PRU) just can’t get any respect. Check out how the life-insurance giant has trailed its main rivals this year:

Snapshot of a Bargain

That’s left PRU trading at just 10.5 times forward earnings and an absurd 7.5 times free cash flow.

With numbers like these, you’d think the company is on death’s door!

Far from it. Third-quarter earnings per share (EPS) hit $3.01 a share, up 13% from a year ago and smashing the Street’s expectations. Revenue jumped more than 10%.

PRU’s focus on retirement (its Retirement Solutions and Investment Management business chips in the bulk of its profit) sets it up to cash in nicely as the baby boomers retire—as they’re doing, to the tune of 10,000 every day.

Here’s something else I love: management knows how to bargain-hunt the company’s own stock. Look at how PRU issued shares earlier this year, with the stock on the rise, then bought them back (resulting in fewer shares outstanding) as it dipped this fall:

Management Puts On a Buyback Clinic

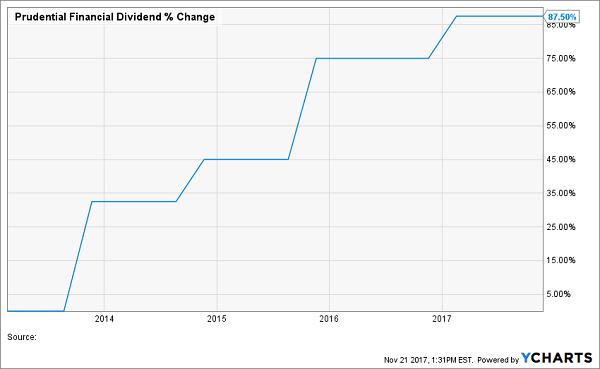

And if you prefer cash over buybacks, PRU has you covered: the stock yields 2.7% now, and this company has dividend growth in its DNA:

A Shareholder-Return Machine

The payout is hardly a burden, eating up just 21% of earnings, so more big hikes are on the way.

“Forever Stock” No. 4: Profit Alongside the CEO

I flagged Penske Automotive Group (PAG), owner of car and truck dealerships across the US, Canada and Western Europe, as a stock with huge upside in a September 25 article.

It’s risen 1.5% since, but it’s just getting started.

How do I know?

Because the CEO, famed automotive entrepreneur Roger Penske, snapped up a cool $50 million of shares just over a month ago, on October 20.

At times like these, it pays to remember the words of legendary investor Peter Lynch: “Insiders might sell their shares for any number of reasons, but they buy them for only one: they think the price will rise.”

Penske sees the same thing I do: a company firing on all cylinders. In the third quarter, record unit sales sent revenue up 7.2%, to $5.5 billion. EPS soared 6.8%, to $1.10.

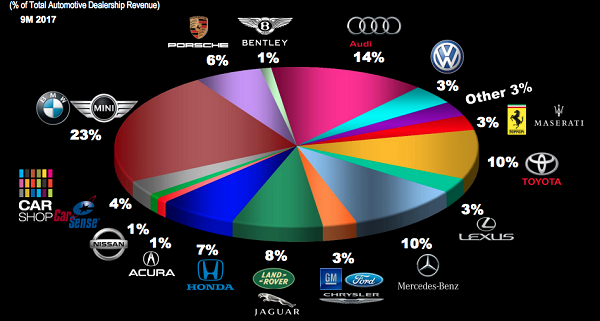

This is one of the most diversified car stocks there is. PAG peddles a huge number of brands, without too much reliance on a single one:

If It Has a Hood Ornament, PAG Sells It

Source: Penske Automotive Q3 investor presentation

Yet first-level investors refuse to notice of the company’s strengths. Not the least of those is its used-car business, which keeps the overall top line growing when new car sales flatten out. In Q3, PAG sold 25.4% more secondhand rides, offsetting a 2.5% decline in new-car sales.

But the first-level crowd’s ignorance is fine by us—it gives us a chance to grab PAG cheap, at just 10.8 times forward earnings.

Finally, there’s the dividend, which yields 2.7% and has risen every single quarter for six years running. With sales and profits surging and the payout taking up just 29% of PAG’s last 12 months of profits, there’s no chance of that slowing down, either.

Revealed: The 7 “Must Have” Dividend-Growth Stocks for 2018

My top 7 dividend-growth stocks for 2018 just came out—and I’ve put them in a new Special Report I want to give you now.

These 3 sleeper picks are so boring they’d put Warren Buffett to sleep! But he’d still approve, because they have 3 advantages the competition can’t match:

- Soaring earnings and free cash flow backed by easily understandable businesses;

- Microscopic payout ratios, to keep their double-digit dividend hikes coming; and

- High barriers to entry, so they spend more time building their high-margin products—and less time fending off predators like Amazon.com (AMZN).

I consider these 3 stocks nothing less than the perfect businesses.

But you’ll never hear about them in the financial media, obsessed as it is with shiny baubles like the Tesla (TSLA) self-driving truck and bitcoin, or speculating on whether tax reform will make its way through Congress.

So what stocks am I talking about here?

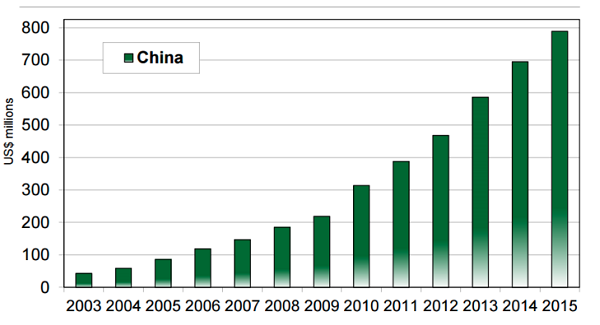

One of these companies makes hot water heaters for the Chinese market, which sounds pretty sleepy until you hear its CEO say he expects 15% annual sales growth for the foreseeable future.

It’s easy to see why: Chinese demand for hot water is soaring along with the size of its middle class:

An Unstoppable Trend

This company’s dividend has nearly tripled in the last 5 years, and its soaring free cash flow means there’s another big hike in store—likely in January, when it usually announces its next increase. So you’ll want to make sure you buy before then.

Here are 3 other picks you’ll discover in this must-have Special Report:

- This stock has boosted its dividend payments more than 800% over the past 4 years and has at least another decade of double-digit growth left in the tank!

- A “double threat” income-and-growth stock that rose more than 252% the last time it was anywhere near as cheap as it is now!

- A 4.3% payer that raises its dividend more than once a year—and will double its payout by 2021 at its current pace!

Your special report is waiting for you now. Simply click here to get your copy and discover the names, tickers, buy prices and my complete analysis of these 7 dividend growers.