Legendary investor Peter Lynch was fond of saying that corporate insiders may sell their shares for a variety of reasons (estate planning, divorce, sending the kids to college). But there’s only one reason they buy – because they think the price is going up.

Insiders at dividend growers have one more reason, however – they obviously believe their payout is going up, too.

Which means when we’re looking for the next dividend accelerator and its 100% upside, we should consider insiders’ favorite payouts. Here are five candidates with big dividend growth and heavy insider buying:

Western Refining (WNR) CEO Jeff Stevens just picked up 100,000 shares last week for a cool $2.3 million. Obviously he believes his firm’s 6.6% forward yield – just months off its all-time high – is secure:

The CEO Buys His Own Big Yield

And the yield’s bull move isn’t entirely due to a sagging stock price. Over the last three years, the firm has increased its payout by 72.7%. Its free cash flow has been positive the entire time (even with oil’s decline) with plenty of room to cover its payout.

And when WNR has extra cash as it often does, it has a tendency to dish it back to shareholders in the form of a special dividend. With three in the last four years, perhaps the CEO senses the next one is approaching.

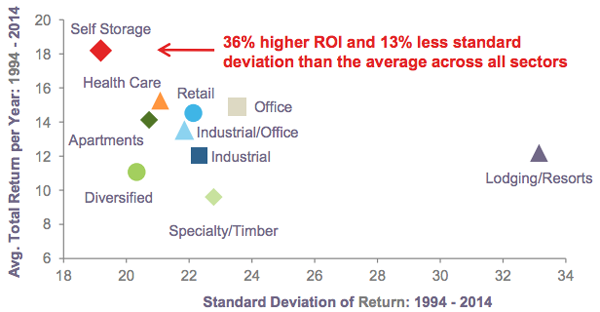

Execs at CubeSmart (CUBE) are taking advantage of the rare pullback in self-storage stocks. From 1994 to 2014, self-storage was the place to be for big, steady gains. These stocks delivered 18% returns gains with the least amount of volatility (or price gyrations, as shown by their low standard deviation of return below) in the REIT world:

Self-Storage Has Been the Place to Be

Stocks that deliver 18% each year without much drama become quite popular with investors over time. As a result, even though these firms pay out the majority of their cash flow as dividends, their yields rarely exceed 3%. CUBE, which has tripled its dividend over the last five years, now boasts a forward yield above 3% for the first time in years.

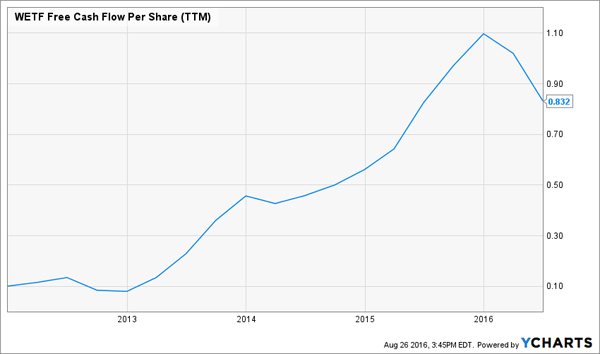

WisdomTree Investments (WETF), purveyor of ETFs, is off its recent highs by 55%. Evidence of an oversaturated ETF market turned one of the hottest stocks of 2015 into one of the dogs of 2016. But some insiders are taking the other side of the “death spiral” trade.

WisdomTree pays a quarterly $0.08 dividend good for a 3.3% yield. In November 2015, it issued a big $0.25 special dividend that almost marked the exact top in the firm’s share price. The company is still generating plenty of cash flow to cover its current dividend, but the trend is now down:

Was 2015 “Peak ETFs” for WETF?

It’s hard to see these insiders doing anything more than perhaps speculating on a favorable exit.

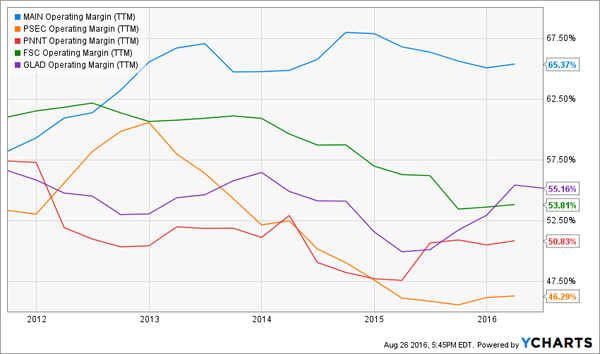

Regular readers know my feelings on business development companies (BDCs) – they are usually externally managed yield traps that pay big dividends but grind down your capital at an equal rate.

Best-in-breed BDC Main Street Capital Corporation (MAIN) is an exception. While its industry at large is known for bloated expenses that eat into income, MAIN keeps itself lean and its profit margins fat:

MAIN’s Industry Leading Margins…

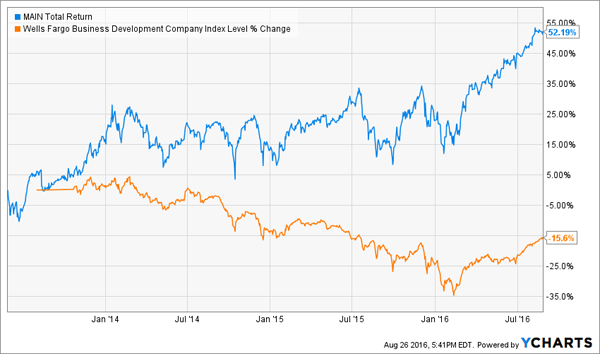

… Help Defy BDC’s Losing Streak

Continued excellence has come at a price for new investors, who currently pay a 62% premium to MAIN’s net asset value (NAV) – a rarity in an industry that has consistently traded at a discount to NAV.

But MAIN appears worth it, and insiders agree. They’ve been heavy net buyers over the past year, purchasing 300,000 shares while selling just 75,000. Insiders currently own 6.5% of the firm.

Beyond these promising insider love-fests, I like 3 dividend stocks even better at the moment. They are my best buys right now.

No matter what happens with the election, Europe’s economy or China’s central planning, there’s one sure bet in the investing world – dividend growth investing is the only reliable retirement strategy.

These corporate insiders know it, which is why they’re loading up on their own shares. These 3 issues are under the radar at the moment – hence the buying opportunity.

It won’t last for long. Despite Janet Yellen’s jawboning about one more measly rate hike, yields are going to stay low for a long time. (It’s why McKinsey & Co. recently concluded investors will be lucky to net 4% over the next 20 years.)

Any income will be at a premium, with dividend growth the undisputed king. In a world averaging 4% returns, a high upside stocks paying 3% in cash with double-digit annual raises is a no brainer. These hidden gems will be uncovered soon – preferably by you! Click here and I’ll share my 3 favorite dividend growth plays with you, including company names, tickers and best buy prices.