I hate to say it, but right now, thousands of investors are putting their portfolios on autopilot right when they need to take control the most.

I’m talking about the boom in “passive” investing, or bypassing stock picking and plowing your cash into low-fee exchange-traded funds (ETFs) instead.

Some income-starved investors are going further, piling into ETFs that hold stocks with either above-average yields or strong dividend growth.

A Brilliant Strategy … Until It Isn’t

In theory, it’s a smart move. After all, companies that pay—and better yet regularly hike—their dividends have a history of outperforming stocks with no payout at all.

But there’s a problem: overall dividend growth is slowing, and faster than most investors think.

According to S&P Dow Jones Indices, US companies collectively hiked their payouts by $6.0 billion in the third quarter (net of cancellations).

That sounds great … until you realize it’s down from $7.3 billion in the second quarter and way down from $10 billion a year ago.

Worse, the number of companies slashing their payouts jumped 55.5%, to 667, in the 12 months ended September 30.

Here’s where that gets risky for investors: many dividend ETFs use formulas that put a lot of emphasis on historical yields and payout hikes when they’re forecasting future growth—a backward-looking approach that could easily backfire when payout growth hits the skids, as it clearly is today.

Just look at the history.

The last time payout growth came under pressure, during the financial crisis, one of investors’ favorite dividend ETFs, the Vanguard High Dividend Yield ETF (VYM), saw its payout nosedive 24% on an annualized basis, from $1.44 in 2008 to $1.09 in 2010.

The problem? VYM tracks the FTSE High Dividend Yield Index, which puts dividend yield first and foremost, with less emphasis on the fundamentals backing those yields.

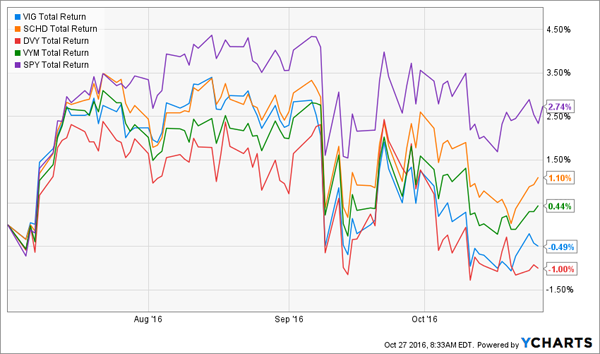

Already, dividend ETFs are creaking under the strain: even though most have beaten the S&P 500 year-to-date (including VYM and three more I’ll warn you about shortly), they’ve trailed the benchmark index since the start of the third quarter:

The bottom line? If you want high, safe yields and strong dividend growth at a reasonable price, there’s still no replacement for a carefully built portfolio of individual stocks.

But if you still want to hold dividend ETFs, do your portfolio a favor and stay away from VYM and these three, or sell them if you already own them.

3 More Wobbling Dividend ETFs to Sell

The Schwab US Dividend Equity ETF (SCHD) yields 2.8% today and tracks the Dow Jones US Dividend 100 Index. It’s also one of the cheaper dividend ETFs to own, with a management fee of just 0.07% of assets.

SCHD’s formula is a little more involved than those of most dividend ETFs: the Dow Jones US Dividend 100 Index includes companies selected based on debt to cash flow and return on equity, as well as current yield and dividend growth.

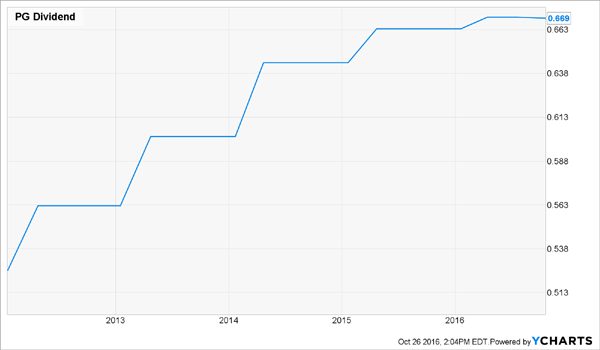

Too bad that formula has driven the biggest slice of the fund’s portfolio—23.3%—into big-cap consumer stocks such as Procter & Gamble (PG), the ETF’s third-biggest holding.

That’s a problem, because as I wrote in August, small, locally based companies are draining sales away from these behemoths, leaving them with only one way to grow profits: cut costs—because their sales are sliding.

In P&G’s case, that’s translating directly into fading payout growth:

Despite that, many consumer staples stocks still trade at overstretched multiples to earnings. That alone is a good reason to leave SCHD on the shelf.

DVY: Overcharging and Underdelivering

Plenty of investors are drawn to dividend ETFs because of their low management fees, forgetting that these fees still add up over time. That’s not the case with stocks, where you pay a one-time commission of as little as $4.95 when you buy or sell.

Worse, some of the most popular dividend ETFs aren’t even cheap!

Like the iShares Select Dividend ETF (DVY), which charges 0.39% of assets annually, or nearly six times what the Schwab fund charges. You do get a higher yield, however. At 3.2%, it’s well ahead of the S&P 500’s 2.2% average.

The bigger payout comes from DVY’s focus on higher-paying sectors, like utilities, which make up 29.6% of the portfolio. But that’s an even higher—and more dangerous—concentration than the Schwab fund! Because despite their recent pullback, America’s biggest utilities still have more downside than up.

Consider NextEra Energy (NEE), DVY’s sixth-largest holding. Right now, NEE trades at 22.6 times earnings, way over its five-year average of 17.8. Put another way, the share price would drop 21% if it simply reverted to that level.

Worse, the stock’s current yield sits at 2.7%, just a hair above NEE’s all-time low of 2.5%.

Unfortunately, in reaching for yield, the iShares Select Dividend ETF forgoes dividend growth, one of the most reliable drivers of stock-price performance. The result? The S&P 500 has crushed it in the 12 years since inception:

It’s true that when you factor in dividends, DVY’s total return comes close to matching that of the S&P 500 in the same timeframe. But that raises another question: why would you bother when you could have just bought the SPDR S&P 500 ETF (SPY) and saved on the fees?

VIG: Swimming Against the Current

The Vanguard Dividend Appreciation ETF (VIG) takes the opposite approach of DVY, placing less emphasis on current yield (it pays around 2.1%) in favor of companies with strong dividend growth. It’s also cheaper, with a management fee of just 0.13% of assets.

This strategy is better than DVY’s, and it’s helped VIG outrun the S&P 500 since inception a decade ago. But I’m worried the fund won’t be able to keep the pace up much longer.

That’s because VIG tracks the NASDAQ US Dividend Achievers Select Index, which consists of 185 stocks that have raised their payouts in each of the past 10 years.

It’s both a backward-looking approach and a narrow set of criteria, and there’s no guarantee it’ll help VIG find the strong dividend growers it needs to keep its share price rising as overall dividend growth ticks lower.

Already, some of its top 10 holdings have payout ratios (or the percentage of earnings paid out as dividends) higher than the 50% I like to see in a stock, such as Coca-Cola (KO), at 77%, McDonald’s (MCD), at 67% and PepsiCo (PEP), at 63%.

Revealed: My Crash-Proof “No-Withdrawal” Portfolio

Just imagine if you were retired and relying on the Vanguard High Dividend Yield ETF for income during the financial crisis.

You would have watched your income shrivel by 24%! And if you’re like most retirees, you would have been forced to sell shares to close the gap, compounding your misery by locking in big losses.

That’s a nightmare scenario if there ever was one.

So it was with 2008—and the next panic—in mind that I crafted my “no-withdrawal” portfolio. It delivers safe, reliable 7.4%, 8.0% and 9.4% yields right out of the gate, letting you retire on dividends alone, without ever having to tap your capital!

Think about that for a moment: when the next crash hits, you could sail above it all, calmly collecting your dividend checks and not having to sell a single stock until the market rebounds.

Most people know this is the right way to invest for retirement. But they don’t know where to find the reliable 7.0%+ yielders they need to make it happen.

One thing you can’t do? Follow the dividend ETF model and rely on blue chips, because they just don’t pay enough.