Britain’s out – should you care? It depends on what’s in your portfolio today.

Here’s a five-point checklist to help you Brexit-proof your nest egg. There’s no shortage of noise floating around about the potential ramifications. Let’s separate the “first-level” headline worries from the second-level realities – and make sure your portfolio is set to thrive regardless of the nonsense coming out of Europe.

Reality #1: Interest Rates Here Aren’t Going Anywhere

Regular readers know I’ve been skeptical of the Fed’s “tough talk” about raising rates ever since it started. Perfectly good high paying issues have been pummeled by their empty threats of sustained hikes, providing contrary-minded income investors like us with excellent buying opportunities.

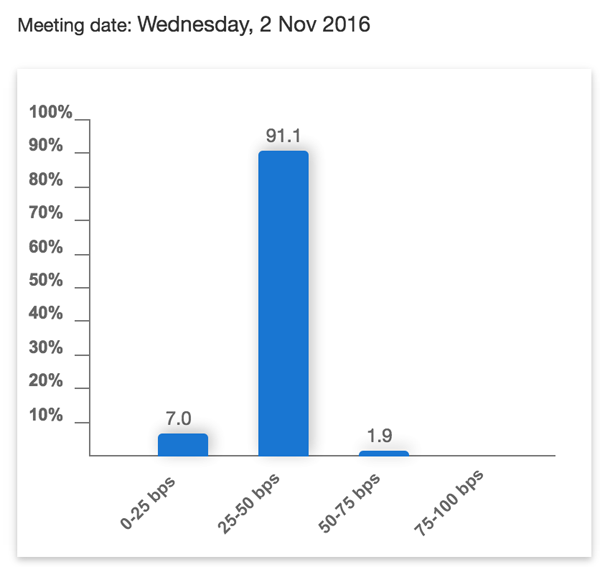

The “smart money” now agrees that rates aren’t moving. Traders betting via the Fed Funds futures market are now pricing in no rate hike until 2018. And how’s this for a twist – they’re now wagering that a rate cut is more likely than a hike later this year! Here’s the current November spread:

A Rate Cut Now More Likely Than a Hike!

The takeaway? With 91% of wagers betting on “no hike”, stocks and funds previously punished for rate hike worries now have the “all clear” signal for at least 18 months.

And let’s be honest – we can probably extend the green flag into the foreseeable future beyond that, as any meaningful series of rate raises would likely break the debt-laden economy once again. The Fed knows this, of course – which is why they have elected to jawbone about rate hikes rather than actually raise them.

Reality #2: Secure High Yield Looks Good, Again

The case against high yield in the face of rising rates was weak from the start. The theory was that there would be serious competition to high yield from safe fixed income vehicles like Treasuries as rates rose. Now that attractive yields on U.S. paper are once again a pipe dream at best, the “next best bonds” will once again move into the spotlight.

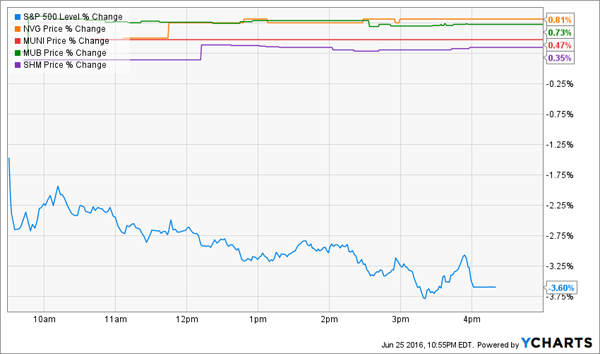

For example, municipal (or muni) bonds already looked good. At large, they rarely default and enjoy tax-free status. If you choose your muni investment vehicles wisely, you can earn tax-advantaged 6% yields without stock market volatility.

High earners took note after the Brexit vote, realizing that 6% translates to a 10%+ yield equivalent for those in the top Federal tax bracket. They sold most of their stocks – and bought munis instead:

Munis Back in Vogue

Reality #3: REITs Look Especially Good

Real estate investment trusts (REITs) have been weighed down by rising rate worries too. The first-level types fretted about competition along with a lack of cheap money for REITs to finance new deals.

The party is back on for these issues, just when they are finally starting to get the mainstream respect they deserve. As we discussed recently, a cool $100 billion or so is gearing up to chase these soon-to-be-hot issues.

Since its 2004 inception, the Vanguard REIT Index ETF (VNQ) has crushed the broader market – returning 192% including dividends versus just 89% for the S&P 500. The market gods have at last taken note – this September, Standard & Poor’s will promote REITs to their very own sector for the first time.

Which means NOW is the best time to buy them, because before it’s official, large funds will be shoveling cash into REITs as they attempt to “front run” the index. JP Morgan & Chase reports that the desire for “equal weight” portfolios will send $100 billion or so into the sector.

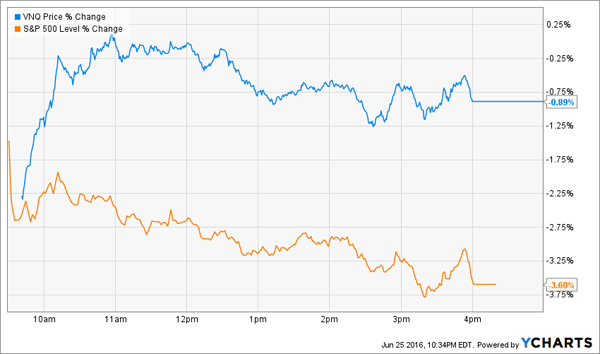

VNQ held up quite well in Friday’s bloodbath:

Brexit? U.S. REITs Don’t Care

While REITs at large look good, certain niches – such as health care – look really good. Here’s how four of the largest healthcare REITs by market cap performed on Friday – three of them actually finished UP on a day that that S&P 500 plunged 3.6%!

Reality #4: Closed-End Funds (CEFs) Got Their Groove Back

Closed-end funds, or CEFs, had the same interest rate overhang. They tend to juice their return with leverage which benefit from low rates. The prevailing theory, as with REITs, was that higher rates would harm CEFs.

It sounds good on paper but that wasn’t the reality for CEFs during the last meaningful rate hike cycle (2004-06). I checked the historical performance of three prominent funds with long track records: the Gabelli Dividend & Income Trust Fund’s (GDV), the Calamos Strategic Total Return (CSQ) and the Eaton Vance Limited Duration Income Fund (EVV). All three outperformed the market during Greenspan’s aforementioned run:

Higher Rates No Problem for Top Closed-Ends 2004-06

I expect we’ll see more money chasing these high paying investment vehicles quite soon.

Reality #5: But Choose Your CEFs Wisely

Why didn’t all CEFs get a lift post-Brexit? Those that own stocks suffered along with equities. If the stock market kicks off a summer swoon, they may continue to flounder.

That’s why I prefer to have my CEFs relatively disconnected from the broader market. I like funds that focus on niches that will generate income no matter what the broader markets do.

My three favorite CEFs are “slam dunk” income plays that pay 8.0%, 8.4% and even 11% dividends. Plus, they trade at 10-15% discounts to their net asset value (NAV) today. Which means they’re perfect for your retirement portfolio because your downside risk is minimal. Even if the market takes a tumble, these top-notch funds will simply trade flat … and we’ll still collect those fat 8% to 11% yields.

Most likely, they’ll jump 10-15% to close the “free money” discount … and we’ll still collect those fat dividends!

It’s only a matter of time before other investors ditch dangerous stocks and find their way over to these “slam dunk” income plays, so the time to buy is now, while they still trade at deep discounts to NAV.

Click here to get the complete story and the names of these three rock-solid retirement picks now.