The suits at Merrill Lynch say you need $738,400 to retire well.

Let me explain why they’re dead wrong. You’ll actually need a lot less than that.

I’m going to show you a simple way to bankroll your golden years on 32% less. That’s right: I’m talking about a fully paid for retirement for around $500,000.

Got more? Great. I’ll show you how you can retire filthy rich on your current stake.

Plus my “no-withdrawal portfolio” will also let you live on dividends alone—without selling a single stock to generate extra cash.

As I’ve written before, this approach is a must if you want to safeguard your retirement from the next market calamity.

The Power of Monthly Dividends

While we’re at it, let’s also set up a smooth income stream that rolls in every month, not every quarter like the dividends you get from most blue-chip stocks.

You probably know that it’s a pain to deal with payouts that roll in quarterly when our bills roll in monthly.

But convenience is far from the only benefit you get with monthly dividends. They also give you your cash faster—so you can reinvest it faster if you don’t need income from your portfolio right away.

More on that a little further on. First I want to show you…

How Not to Build a Solid Monthly Income Stream

When it comes to dividend investing, many “first-level” investors take themselves out of the game straight off the hop. That’s because they head straight to the list of Dividend Aristocrats—the S&P 500 companies that have hiked their payouts for 25 years or more.

That kind of dividend growth is impressive. And some of these names do have a place in your portfolio—including 3 Aristocrats I pounded the table on in early June.

But here’s the problem: these folks are forgetting that companies don’t need a high dividend yield to join this club—and without a high, safe payout you can forget about generating a livable income stream on any reasonably sized nest egg.

Worse, you could be forced to sell stocks in retirement—maybe even into a 2008/09–style nosedive—just to make ends meet.

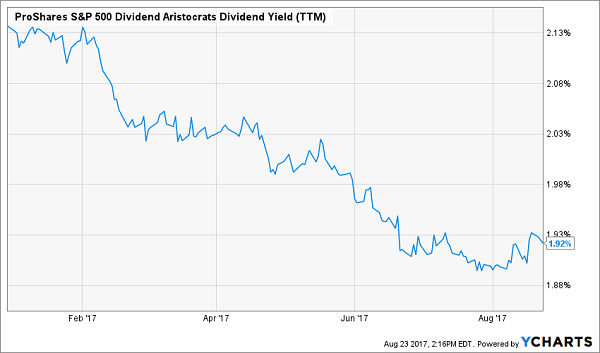

That’s a nightmare for any retiree, and leaning too hard on the so-called Aristocrats can easily make it reality: the ProShares S&P 500 Dividend Aristocrats ETF (NOBL), which holds all 51 Aristocrats, yields a pathetic 1.9% as I write, exactly the same as the S&P 500 average!

Worse, that yield is in free-fall as stocks grind higher:

The Aristocrats’ (Not So) Incredible Shrinking Yield

Solid Monthly Payers Are Rare Birds…

You can certainly build your own monthly dividend portfolio, and the advantage of doing so is obvious: you can target companies that pay much more than your average Aristocrat’s paltry sub-2% payout.

Trouble is, only a handful of regular stocks pay in any frequency other than quarterly, so we’ll have to patch together different payout schedules to make it happen.

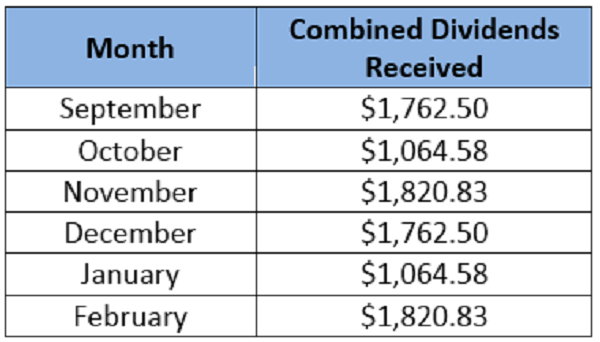

To do that, I’ve swung back to the Aristocrats, scanning for a combo of above-average yields and payout schedules that line up. Here’s an “instant” 6-stock monthly dividend portfolio that fits the bill:

- AT&T (T) and AbbVie (ABBV)—two of the highest-yielding Aristocrats, with payouts of 5.2% and 3.6%, respectively—pay in February, May, August and November.

- Target (TGT) and Chevron (CVX), with payments in March, June, September and December.

- Sysco (SYY) and Wal-Mart Stores (WMT), with payments in January, April, July and October.

Here’s what $500,000 evenly split across these six stocks would net you in dividend payouts over the next six months, based on current yields and rates:

You can see the consistency starting to show up here, with payouts coming your way every single month, but they still vary widely—sometimes by nearly $800 a month!

Of course, the bigger problem is that we’re pulling in just a 3.7% average yield, which will only get us to $18,600 in income on our $500,000 nest egg. That’s less than your local Starbucks barista makes!

We need to do better.

…But It Pays to Own Them

Here’s where you need to step away from regular stocks and fish in lesser-known corners of the market—places where high yields and monthly payouts abound.

One of my favorites? Real estate investment trusts (REITs) a special kind of company that owns rental properties—everything from shopping malls to senior-care facilities.

Here’s the upshot: the IRS lets REITs skip out on income taxes if they pay out most of their earnings as dividends. That means fatter dividend checks for you and me. Better yet, monthly payouts are more common in the REIT world.

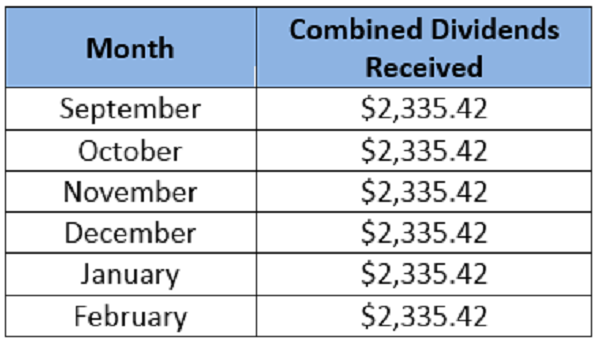

So let’s go ahead and build a monthly dividend REIT portfolio with 4 names that should be on any income hound’s radar:

- Industrial landlord STAG Industrial REIT (STAG), a 5.0% yielder I recommended on August 14.

- Long-term care facility owner LTC Properties (LTC), with a 4.8% payout.

- Apple Hospitality REIT (APLE) a hotel operator that pays 6.7%.

- EPR Properties (EPR), owner of theaters and entertainment complexes across the US—and a fat 6.0% payout.

Here’s what you could expect every single month for the next six months if you dropped $500k into these four, again based on current yields and rates:

That’s as smooth an income stream as you’ll ever see! And it’s certainly better than our cobbled-together Aristocrat portfolio, getting us up to around $28,000 a year in income (or a 5.6% average yield) on our $500,000 cash pile.

There’s one problem, though: that $28,000 is still below the $40,000 or so most folks would need to retire on dividends alone.

Which brings me to…

Your Best Move Now: 8% Dividends AND Monthly Payouts

This is where my “No-Withdrawal Portfolio” comes in. With just $500,000 invested, it’ll hand you a rock-solid $40,000-a-year income stream. That’s an 8% dividend yield … and it’s easily enough for most folks to retire on.

The best part is you won’t have to go back to “lumpy” quarterly payouts to do it! Of the 6 income studs in this unique portfolio, 4 pay dividends monthly, so you can look forward to the steady drip of $3,333 in income, month in and month out—give or take a couple hundred bucks!

I’m ready to give you everything you need to know about this life-changing portfolio now. All you have to do is CLICK HERE and I’ll share my proven monthly-dividend strategy, plus the names, tickers and ALL of my research on these 6 income wonders!