Is the next market brushfire right around the corner? And are investors in denial about it?

If recent moves in the CBOE Volatility Index (VIX) are any indication, the answer to both questions could be yes.

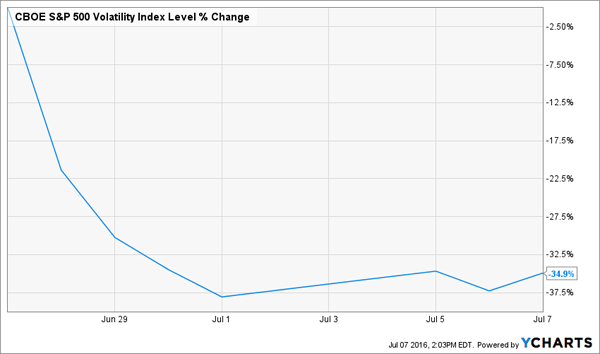

The market’s so-called “fear indicator” plunged 40% in the week following the Brexit vote—its largest-ever drop—as options traders bet the worst is behind us. The VIX has moved back up only slightly since.

But don’t break out the bubbly yet. Because if anything, this sudden outbreak of investor contentment—and the disappointment that’s sure to follow—sets the stage for more, not less, volatility to come.

The yield on the 10-year Treasury is the canary in the coal mine. Earlier this week, it hit a record low as—despite the drop in the VIX—investors went on the hunt for safety post-Brexit.

Speaking of Brexit, negotiators haven’t even started talking yet, so there are plenty more surprises to come on that front. And I won’t even get into the U.S. presidential race, which continues to descend into farce as it grinds toward its end.

Something else to watch out for? Seasonality.

According to the Hulbert Financial Digest, from 1896 through 2014, September was the worst month for stocks, with the Dow posting an average loss of 1.06%, compared to an average gain of 0.75% for all the other months.

Before we go further, let’s be clear on one thing: just because September is often lousy for stocks doesn’t mean you should vote “leave” on the market in August.

That’s because, as I showed you when we debunked the flawed “sell in May” strategy, patterns like these don’t always repeat. For example, if you were out of stocks last September—the one immediately following Hulbert’s study—you would have missed out on a 1.4% gain in the S&P 500.

However, September’s tendency toward weakness does make now a great time to buy the four investments below, which profit whether the market (and the economy) goes up, down or sideways.

Three of them are top-quality dividend-growth stocks, which, as I’ve written before, are a proven way to build lasting wealth. Study after study has shown that dividend growers deliver higher long-term returns than steady dividend payers and stocks that pay no dividends at all.

I’ll give you three great picks that hold their own when the markets fall out of bed in a moment. First, I want to talk about an even more reliable asset class few investors take advantage of: municipal bonds.

Cut Your Portfolio’s Volatility and Collect a Tax-Equivalent 10% Yield

Municipal bonds, or “munis,” have several advantages, including the fact that many enjoy tax-free status, and they almost never default. According to Moody’s Investors Service, just 0.03% of muni bonds have defaulted since the 2008 meltdown.

Trouble is, a five-year municipal bond yields just 0.98% today, which is actually a loss with inflation factored in. That’s why I prefer to invest in muni bonds through closed-end funds (CEFs), which offer a heady mix of high, tax-advantaged yields and low volatility.

The higher yields come from their use of leverage—borrowing money at low rates to invest in municipals with higher rates. Sure, leverage can be dangerous, but unlike exchange-traded funds, CEFs have active managers who make sure the portfolio is invested in safe securities.

But which muni-bond CEF should you buy?

Near the top of your list should be the Nuveen Enhanced AMT-Free Municipal Enhanced Opportunities Fund (NVG), which has three huge pluses that make it more than worth a look.

One is that muni CEFs like NVG tend to move independently of the market, so they’re a great way to add ballast to your portfolio. NVG, in fact, boasts a beta rating of minus 0.07, meaning it has a slight tendency to move in the opposite direction of the S&P 500.

Second is its gaudy 5.6% dividend yield and the fact that it pays dividends monthly. Finally, NVG’s distributions are exempt from federal income tax, so if you’re in the top federal tax bracket, say, your “real” yield is closer to 10%.

So if you haven’t discovered the wonderfully boring world of municipal-bond CEFs, now’s the time to do so—starting with NVG.

Now here are my…

3 Top “Steady Eddie” Stock Buys

CVS Health (CVS) is perfectly positioned to profit from a demographic trend that isn’t going anywhere, despite Brexit, the Fed or the outcome of the presidential race: the aging of the baby boomers (more on that below).

The company runs America’s largest drugstore chain, a pharmacy-benefit-management business and 1,100 in-store medical clinics.

One way to judge a stock’s resilience is to look at how it’s performed in the past, and there’s no better petri dish than the 2008/09 financial crisis. CVS fell, along with most stocks, from the market’s 2008 high on January 2 of that year, but it recovered almost 10 months faster than the S&P 500, retaking its January 2, 2008, level in late December 2011.

While they were waiting, CVS investors enjoyed a quarterly dividend that rose steadily throughout the meltdown and has continued to do so at a breakneck pace. Since July 2008, the payout has soared 608%—a fact that’s masked by the stock’s 1.8% current yield.

One other factor puts a floor under the stock price: CVS’s ongoing buybacks, which boost earnings per share because they cut the number of shares outstanding. In the past five years, the company has cut its share count by more than 20%.

The topper? The stock’s forward price-to-earnings ratio clocks in at 16.5, a big discount to its industry, at 24.3.

Verizon (VZ) is another strong dividend grower that can help ground your portfolio in whipsawing markets. That’s partly due to its beta rating of just 0.26, meaning the stock is 74% less volatile than the S&P 500, historically.

The company’s ultra-loyal wireless subscribers add to that stability: in the first quarter, its churn rate (or the percentage of clients who cancel) was just 0.96%, compared to 1.1% for AT&T (T) and 1.7% for Sprint (S).

Verizon’s dividend-growth story isn’t as compelling as CVS’s, but its payout’s as safe as they come: like CVS, the telecom giant kept raising its dividend throughout the financial crisis. The current yield is also more attractive, at 4.1%, so you’re starting from a higher base.

Moreover, Verizon’s dividend represents just 48% of its free cash flow, leaving it plenty of room to keep the hikes coming—look for the next one this September—and invest in fast-growing areas like the Internet of Things and online advertising.

Despite a big run-up this year, the stock is still a good value, with a forward P/E of 14.1, below its five-year average and competitors like AT&T, at 14.9, Comcast (CMCSA), at 18.6, and Sprint, at 28.4.

Pfizer (PFE): I hope you jumped on this one when I recommended it on February 29. If so, you’re sitting on a nice 20% total return since then.

If not, don’t worry. There’s still time. The stock’s forward P/E is just 14.5, and it’s another great play on aging baby boomers. The shares yield a tidy 3.4% today, and the dividend’s been growing at a 10% annualized pace over the past five years.

Backstopping Pfizer’s profit—and dividend—growth is the fact that, unlike dangerous drug stocks such as Valeant Pharmaceuticals (VRX), Pfizer’s a big believer in R&D spending. Last year, it poured an incredibly high 16% of its revenue into product development.

One drug to watch? Bococizumab, an experimental treatment designed to both lower cholesterol and prevent heart attacks and strokes. That could give it a big edge over its competitors, which only manage cholesterol levels.

Pfizer’s 3.4% yield is nice—and its payout is rock solid, no matter what happens with the economy and the markets. But what if I told you there’s a way to more than double that yield right now, and at a bargain, to boot?

I’m talking about a safe investment that’s yielding 8.7% today … and it’s riding the same unstoppable demographic shift as Pfizer and CVS.

This company is a real estate investment trust (REIT) that specializes in skilled nursing facilities (SNFs), which provide the highest level of care a person can get while still living independently.

I’m 90% sure you’ve never heard of this hidden gem. It’s a recent spinoff, so just 3 analysts cover it. But with everything this smartly run outfit has going for it, the stock won’t stay off investors’ radar for long.

I’m expecting big things from this one, with payout hikes that will have you yielding 10%+ on your initial investment in no time, plus annual price gains of 10%–15%.

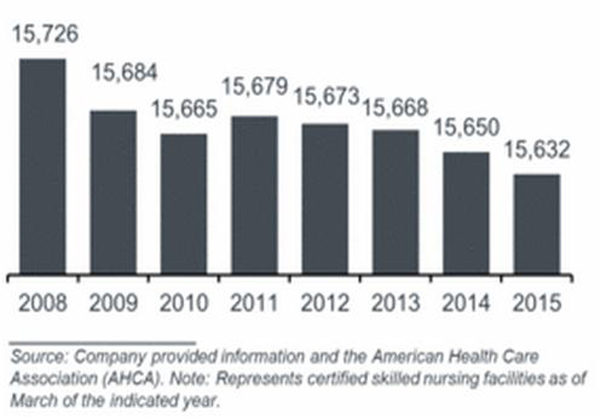

Because here’s the thing about the SNF market: even though demand is soaring, we actually have fewer SNFs than we did in 2009.

This firm is already capitalizing on this situation, and I expect it to announce its first big dividend hike by September.

Don’t miss out. Click here to get the name of the company, the ticker, and two more stocks profiting from the biggest demographic shift in US history.