Forget the trade war. There’s a bigger danger that too many investors (and especially vulnerable retirees) are ignoring today.

That’s the threat of a snap dividend cut—and the massive damage it can do to your income and your nest egg.

More on that—and 4 imminent dividend cuts you need to dodge now—shortly.

Why I’m Sounding the Alarm

First, there are two reasons why folks are sleepwalking along, wrongly thinking all of their dividends are safe:

- The economy is strong, churning along at a 3.1% rate—lulling most folks to think that only the worst companies would be forced to slash payouts.

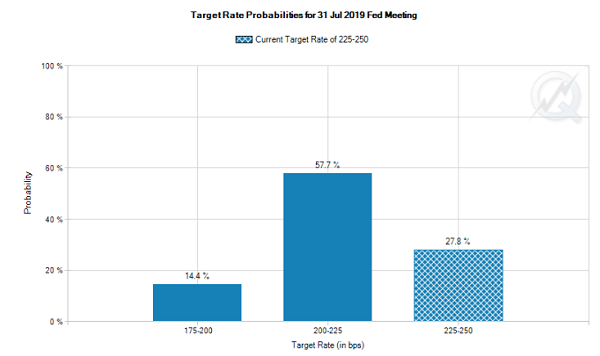

- The Fed’s kabuki theater: After being set on raising rates last year, Fed Chair Jerome Powell is signalling a rate cut. Investors agree: the Fed futures market sees a 66% chance of a rate cut as soon as the July 31 Fed meeting:

Source: CME Group

A rate cut is a plus for dividend payers because lower yields on so-called “safe” investments, like Treasuries, drive more buyers to dividend stocks. And of course, lower rates also cut companies’ borrowing costs.

A Hidden Threat

I’d add a third reason why dividend investors are in denial about the odds of a cut: fewer companies have slashed their payouts this year.

But that’s changing.

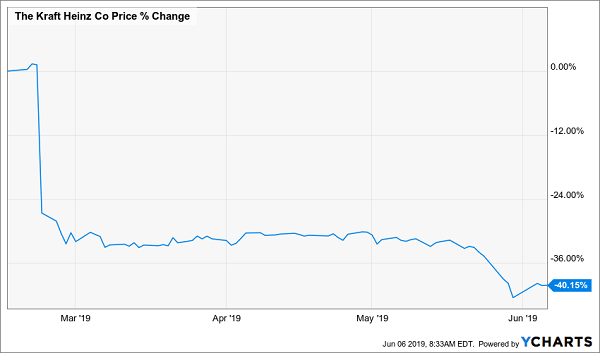

Take Kraft-Heinz (KHC), a “dividend dumpster fire” I’d been warning about for years before it slashed its payout 36% in February. The response was swift and brutal: so-called “steady” KHC crashed 32% in a day—and that was just the start.

A Crippling Loss

Imagine being on the cusp of retirement with your nest egg tied up in this stock! And, like the first few raindrops in a storm, KHC’s cut was swiftly followed by more.

A “Too Good to Be True” Dividend Collapses

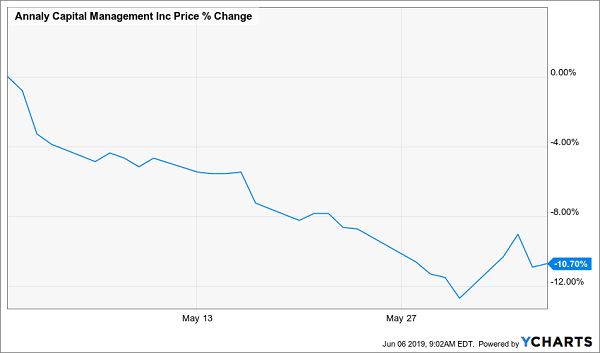

On May 1, Annaly Capital Management (NLY), a real estate investment trust (REIT) with mortgages on commercial and residential properties (and was famed for its massive 13.3% dividend yield), slashed its payout by 17%, triggering a double-digit drop in the share price.

(I told the story of Annaly, and gave my latest advice on mortgage REITs like it, in a June 5 article you can read here.)

Dividend Cut Crushes NLY

Then, just last week, GameStop (GME) got in on the act, cutting its payout entirely (Another cut I called months ago—GME is the Blockbuster of video games, peddling consoles and physical games while more gamers go online.)

The response was predictable:

GameStop Loses a Life

I’m telling you all this now because this is a perfect time to comb through the stocks you own (or those on your buy list) and do a simple dividend “safety check.”

The good news is, you can do it in 3 simple steps. I’ll show you those, and name 4 other deadly dividend stocks you need to sell now (or avoid if you don’t already own them) as we move along.

Dividend-Safety Tip No. 1: Get the Right Payout Ratio

The payout ratio is our first stop when testing a dividend: it’s the percentage of net income a company has paid out as dividends in the last 12 months. So if that percentage is below, say, 50%, you’re good, right?

Not exactly. Because too many people are looking at the wrong ratio!

Trouble is, the net income half of the equation is an accounting creation that can be manipulated and often has little relation to the actual cash a firm is making. To get the real story, we need to look at the free cash flow (FCF) payout ratio.

FCF is a snapshot of how much cash a company is generating once it’s paid the cost of maintaining and growing its business. You calculate it by subtracting capital expenditures from cash flow from operating activities (you can find both figures under the “Financials” tab on Yahoo Finance).

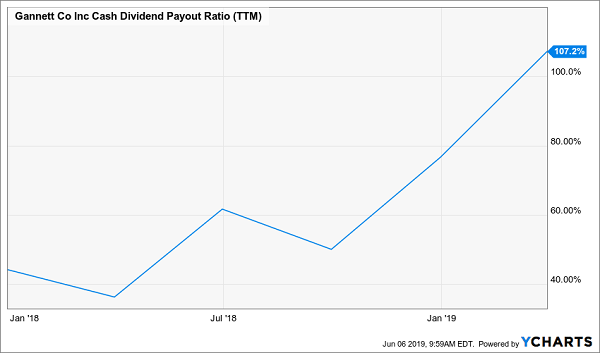

Which brings me to the first dividend that’s almost certainly on the chopping block: the sky-high 8% payout at Gannett (GCI), publisher of USA Today, the Detroit Free Press, Des Moines Register, Rochester Democrat & Chronicle and others.

If you own GCI, you’re already sitting on a 5.5% loss in the past year, while the rest of the market has gained 13%.

That’s bad enough, but over the last few months, GCI has quietly gone from paying a manageable portion of FCF as dividends to paying out more in dividends than it earns in FCF.

GCI’s Dividend: Yesterday’s News?

I first warned you about GCI’s worsening dividend health in January 2018. And things have only gotten worse since.

But investors haven’t been paying attention, especially with the latest GCI news focused on very early talks on a possible merger with fellow newspaper publisher GateHouse Media.

That leaves us with a dividend resting on a deal between two companies in a dying industry, with GCI’s payout accounting for 107% of FCF (and climbing). That’s way too much of a gamble, especially when there are far safer 8% dividends available to us now.

Dividend-Safety Tip No. 2: Cash Flow Is King

Even if you’ve found a stock with a reasonable FCF payout ratio, you’ll want to make sure the underlying free cash flow is stable—or better yet rising—so the payout ratio doesn’t float up into the danger zone, like Gannett’s has.

Because the truth is, just a few quarters of soft FCF can tip the balance fast, and tighten the vice on the dividend before you realize it.

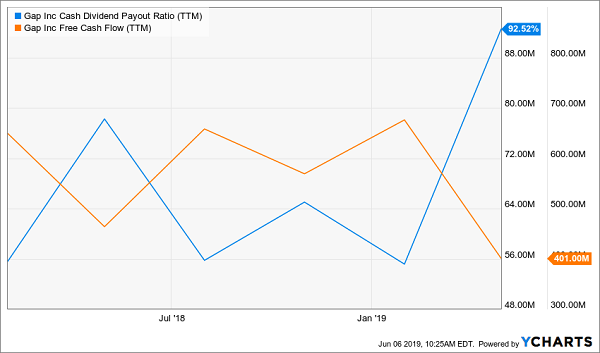

Case in point: Gap Inc. (GPS), payer of a 5.2% dividend. The clothing retailer had a relatively manageable payout ratio—55% of FCF—as of early 2018. Too bad FCF has fallen through the floor since, putting pressure on the dividend:

Noose Tightens on Gap’s Payout

With a terrible earnings report (sales down 2% in the latest quarter and across all three of its main brands: Gap, Old Navy and Banana Republic) and Gap having failed to raise its payout for 15 months (another red flag), this is another endangered payout.

Dividend-Safety Tip No. 3: Stock Screeners Are Terrific Tools …

You can save yourself a lot of work by going with a dividend-safety screen like DIVCON, one of my go-to tools for dividend-stock research.

DIVCON uses a five-tier rating system that provides a snapshot of dividend health for individual companies. It’s offered as a free resource by ETF shop Reality Shares. (You can access DIVCON’s scores for free right here.)

The test combines and weights seven factors (including cash flow, earnings growth and dividend history) to provide a snapshot of a company’s dividend health.

DIVCON 5 is the best bucket. It means the dividend is in good shape, and there’s a very good chance it’ll be increased in the next year.

DIVCON 1 is the danger zone. It means the dividend is more likely to be cut than raised in the next 12 months.

Current “DIVCON 1s” include two other dangerous dividends I’ve been warning about for a while, and am doing so again today: 11.4%-paying Prospect Capital (PSEC), which I last covered in March, and lingerie retailer L Brands (LB), which already cut its payout this year and is still weighed down by an uncomfortably high 73% FCF payout ratio.

… But Don’t Rely on Them 100%

But before you dive into a screening tool like DIVCON, keep in mind that for real estate investment trusts (REITs)—another great place to hunt for big dividends—net income and FCF aren’t the best measures of performance (and dividend safety).

For that, you need to look at funds from operations (FFO), a metric some screeners aren’t set up to deal with, causing them to flag REIT dividends as risky when they’re not (and vice versa).

That just means you have to check REIT dividend safety “the old-fashioned way,” by doing a quick dive into the last four earnings reports and adding up per-share FFO.

This “Pullback-Proof” REIT Pays 8.3%—and It’s Cheap (for now)

But let me save you a few steps, because I’ve uncovered a REIT that’s passed my toughest dividend-safety checks with flying colours!

This commercial landlord is one of those rare “unicorns” you hear about but rarely see: it pays an outsized 8.3% dividend, and its payout is growing like a weed (with 3 special dividends tossed in for good measure).

A Surging 8.3% Income Stream

That begs an obvious question: why would you mess around with perilous payouts like L Brands and Prospect Capital when you could buy this pick, which is begging us to take cash off its hands?

Here’s another bonus of a high, and growing, 8.3% dividend: it keeps pulling investors in, even when the broader market throws a fit. That’s why owners of this stock raked in a double-digit return in 2018, a year most investors would like to forget:

A “Pullback-Proof” Superstar in Action

This commercial lender boasts some of the sharpest minds in the business, and you can bet they’ll be working with us, because they’ve got a lot of skin in the game: insiders own $239 million of equity, or about 12% of the company.

Any serious dividend investor should own this stock, for 3 simple reasons:

- It’s a screaming bargain—but that won’t last, so you’ll want to act now if you don’t want to miss out.

- It survives (and thrives) when market storms hit.

- It yields a fat 8.3% dividend that’s surging (and regularly giving us special dividends).

- Its payout is easily covered by cash flow.

This 8.3%-payer is so steady I’ve made it the cornerstone of my 5-stock “pullback-proof” portfolio, which I’ve built to hold its own in all market weather—and hand you an 8.4% average dividend the whole time!