Is it time to tariff-proof our dividends (again)?

A couple months into the U.S.-China trade tensions, I said the key was to buy dividend-growth stocks: “Payout growth like that is proven to throw an updraft under share prices when the markets get skittish due to any kind of worry: trade spats, terrorist attacks, wars—you name it.”

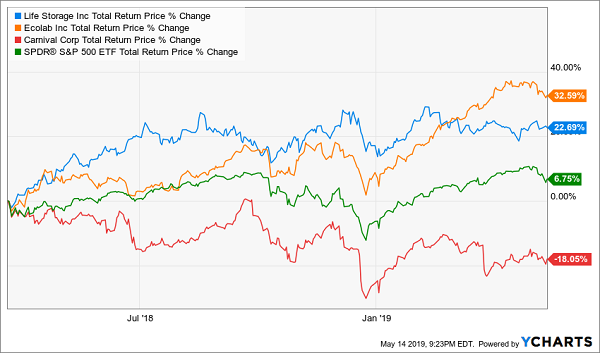

Then I highlighted a trio of dividend growers–Life Storage (LSI), Ecolab (ECL) and Carnival Corp. (CCL)–that looked primed to swim upstream. Unpredictable fuel costs helped weigh on our Carnival pick, but even then, the combined total return of all three selections nearly doubled the S&P 500’s return.

A Winning Tariff-Proof Portfolio

Now, here we are again. The U.S. has ramped up tariffs on China, and Beijing has retaliated. Stocks have plunged into volatility in the early offing. Uncertainty is back.

You and I can focus on the factors that matter, however: dividend growth, high current yields and/or businesses that are mostly China-proof. Let’s get into a new tariff-proof four-pack with 100% price upside or better (powered, as usual, by soaring dividend payouts).

Wendy’s (WEN)

Dividend Yield: 2.2%

I don’t want to linger on burger-slinger Wendy’s (WEN) too long because I highlighted it earlier this month. But it bears repeating as a great way to fend off the Red Dragon.

You can read my bull case on Wendy’s in full here, but in short, it has red-hot dividend growth and a skinflint payout ratio, as well as generally improving operations.

What makes it a specifically compelling play right now is that it’s one of the largest fast-food companies that aren’t really exposed to China. In fact, Wendy’s has precisely zero locations in the country. Malaysia, Japan, the Philippines, Indonesia … check. China? Nada.

Yes, Wendy’s is likely to suffer higher input costs on things such as produce in its salads and on its burgers, but same goes for most of its competitors. But Wendy’s doesn’t have to deal with anti-American sentiment in China – something that could be a drag on the international results of company’s such as McDonald’s (MCD).

AT&T (T)

Dividend Yield: 6.7%

AT&T (T) is a difficult stock to get behind. While it’s a Dividend Aristocrat, its dividend growth has slowed to a crawl, at a mere penny per share for years that put 2019’s boost at a mere 2%. The company’s growth prospects haven’t looked good for a long time.

But I would be remiss to point out that AT&T has delivered a yield this big just a handful of times over the past three decades.

AT&T: A Blue-Chip Business Yielding Like a Dying Retailer

AT&T still isn’t an elite play, but it might be a “making the best of a bad situation” play. You see, the domestic nature of AT&T’s business makes it a smart place to hide while America and China duke it out.

For one, AT&T has no Chinese revenues. And there has been some confusion about the effect on smartphone and peripheral prices like those sold in AT&T stores. Avi Greengart, founder and lead analyst at Techspotential, tells TomsGuide that “parts and materials have just gotten a lot more expensive, but phones and other devices are not subject to the larger tariffs. Most consumer electronics are assembled outside the U.S., so the direct impact here should be fairly low.”

And while AT&T will have a tough row to hoe with the streaming offering it plans to launch in late 2019–it must battle Netflix (NFLX), Amazon.com’s (AMZN) Prime Video, Hulu and Disney’s (DIS) new over-the-top service – it is doing one thing right. AT&T is yanking Time Warner TV shows and movies from the likes of Netflix and stuffing it into its service, weakening its rivals while bolstering its own offering in one move.

Equinix (EQIX)

Dividend Yield: 2.1%

Data center real estate investment trust Equinix (EQIX) has the kind of chart I can’t help but love: One where prices are generally chasing the dividend higher, and there’s still more room for the price to catch up.

Equinix Keeps Booting Up Bigger Cash Payouts

Equinix, for those not familiar, is a colocation provider that boasts nearly 10,000 customers and 341,000 total interconnections across 52 metro areas in 24 countries. It’s the largest global data center company by market share, and it has been swiftly expanding its lucrative enterprise business.

This is absolutely a growth business. EQIX has logged 65 consecutive quarters of increasing revenues, which tops every other company in the S&P 500, and it anticipated 8%-10% in annual revenue growth through 2022.

Its 2.1% yield is nothing special, though it’s largely an effect of a growing share price keeping up with a rapidly growing dividend. EQIX’s quarterly payout has jumped by 45% since it initiated payouts in early 2015–and is only paying out less than half its adjusted free cash flow (AFFO) in dividends, portending plenty of dividend growth ahead. But the stock has rocketed roughly 150% higher in that time, depressing the yield.

This is a great problem to have from a superstar REIT.

Cogent Communications (CCOI)

Dividend Yield: 4.3%

Speaking of growth, let me introduce you to Cogent Communications (CCOI).

Cogent Communications plays in roughly the same sandbox as Equinix. But it’s not a REIT, and while it does provide colocation services, it’s primarily an Internet Service Provider (ISP) that provides businesses with high-speed Internet and Ethernet transport. It’s one of the top networks in the world, and it is indeed worldwide, spanning more than 200 markets across 43 countries.

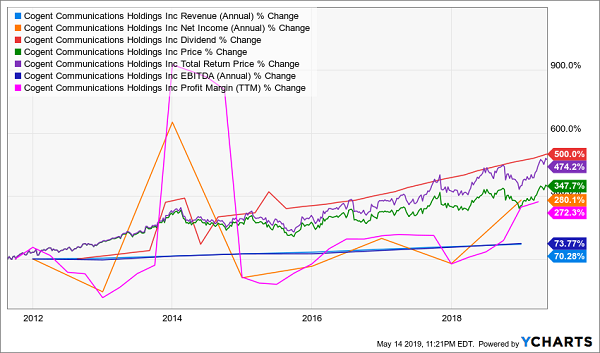

It’s a simply booming business that has helped CCOI expand just about every meaningful statistic you can think of.

- Revenues: $404.2 million in 2015, $502.2 in 2018

- Operating Income: $46.1 million in 2015, $85.6 million in 2018

- Net Income: $4.9 million in 2015, $28.7 million in 2018

- Free Cash Flow: $48.2 million in 2015, $84.0 million in 2018

Cogent Communications Is a Red-Hot Growth Stock, And …

But best of all, it blends a nice current yield above 4% with a stellar streak of dividend increases that recently was extended to 27 consecutive quarters. These aren’t token hikes, either. At its current rate of growth, CCOI will double its early 2015 dividend by the end of this year.

It seems too good to be true, right?

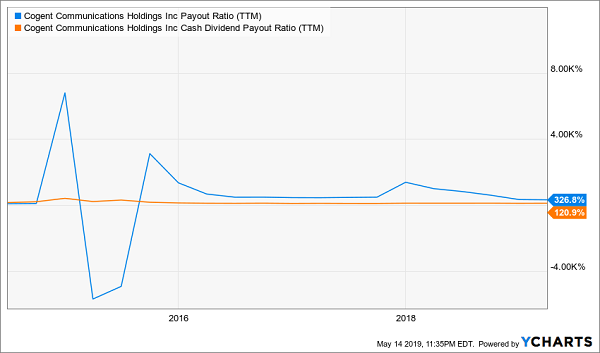

Uh Oh, Payout Ratio

CCOI has a payout problem. It’s not a full-blown panic–yet. But the dividend is by far outstripping its net income, and free cash isn’t enough to tackle the distribution either. In fact, despite the fact that 2020’s expected profits of $1.15 per share should be more than 80% greater than 2018’s, it doesn’t come close to touching its current annual obligation of $2.40 per share.

And that makes me wonder just how reliable this dividend will be down the road.

7 Dividend Stocks That’ll Double Your Money Every Few Years

Dividend growth still is the surest path to trumping the tariff tantrums, but you need the no-doubt picks in the space.

Specifically, you need the dividend growers in my Hidden Yields portfolio.

Since inception, my “HY” portfolio has returned 16.3% per year. This means our inaugural subscribers are well on their way to doubling their money with safe dividend stocks! With patience and persistence, you can enjoy the same types of returns by following our dividend-double strategy.

Today, I want to share seven of my recession-proof “Hidden Yield Stocks” with you.

My research indicates each of these investments could easily pay you 15% per year. That’s enough to double your money in under 5 years. Imagine turning a retirement ‘pot’ of $250,000 into $500,000 … or $500,000 into $1,000,000 … and on it goes.

Imagine no more fear of your savings running dry, no more worrying about wild market swings or crashes, no more risky-bets on penny-stocks or cryptos, and no more penny-pinching in your golden years.

So, if you’re not quite as wealthy as you hoped you’d be, if you wish you had more money in your retirement account, and if you’re looking for safe, secure growth over the next 5, 10, 15, even 20 years – as well as predictable income – this could be the most important investment advice you ever read.