S&P’s new REIT index is officially live – but don’t worry, there’s still a way to front run it!

I’ll get to specific bargains in the sector shortly. First, let’s review the stocks that have already been bid up by investors and money managers looking for exposure to this newly celebrated sector.

Barron’s reported that investors have been using ETFs to invest in REITs, because most individual names – even the sector’s blue chips – aren’t well known by the first-level types.

I believe it, and they don’t need the “s” in ETFs, because the only REIT ETF anyone really knows or buys is the Vanguard REIT Index Fund (VNQ). Since the “sector coming soon” announcement, it’s comfortably outpaced the S&P 500 with barely a Brexit blip!

Investors Rush to REITs via VNQ

The rush to VNQ means the ETF itself must rush to acquire more shares from its constituents. These stocks have benefited handsomely, with four of VNQ’s top five holdings beating the S&P over this time period (and three doing so with authority):

VNQ Then Buys More Shares

Our problem with this bull move? Yields are bid down in the process. Remember, the majority of REIT returns come from dividends (no surprise with 90% of their taxable income required to be paid out to shareholders as distributions). Which leaves dividend growth as the last hope for additional returns when REIT valuations are stretched and yields are low.

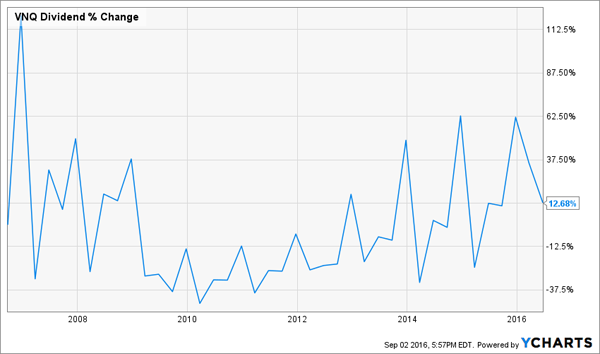

Whether or not dividend growth can be relied upon depends upon your view of the financial world. If you believe nothing bad is likely to happen for awhile, then you’ll be fine. After all VNQ’s dividend increased 54% over the last five years – nothing bad happened, and real estate performed well.

But if you’re worried that something, anything, could go really wrong anytime in the next decade, then broad-based dividend growth won’t cut it. Case in point, VNQ’s dividend is only 13% higher from its mark a full decade earlier:

Barely Better Than a Round Trip

As you probably know I don’t believe one more measly rate hike qualifies as bad news for REITs. This time last year was the best time to buy them, prior to the December rate hike. Plus, the best REITs rolled through the last major series of upticks in rates from 2004 to 2006. There’s no reason to believe it will be different this time if we do happen to swing into a major hike cycle.

But aren’t the best REITs now expensive? No, the largest stocks – namely those owned by VNQ – are the now pricier ones. The ETF pays 4% today, which isn’t bad, but I prefer to see my REIT yields a point or two higher.

My advice? Ignore the blue chip names and tap the recession-proof B-list names. The lesser known names pay more, boast healthy prospects for cash flow (and dividend) growth, and shouldn’t get bogged down by an economic slowdown or even a stock market crash.

Here are three to consider that pay between 5.6% and 5.9%:

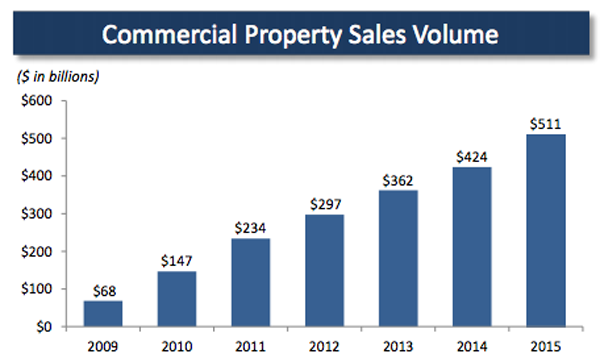

W.P. Carey (WPC) owns and manages commercial real estate, a market that is quietly booming:

WPC’s 5.9% yield is significantly higher than competitor (and blue chip darling) Realty Income’s (O) 3.7% dividend. Since I warned you about O less than a month ago, it’s already down 2.5% – showing that, once again, valuations do matter.

Apartment landlord Preferred Apartment Communities (APTS) is capitalizing on the millennial-driven trend to rent for longer (or perhaps forever) as the baby boomers downside their empty nests in tandem. APTS has increased its payout by 62% over the last five years, and demand for its rental units could actually increase further if a recession sends home owners packing. Shares yield 5.8% today.

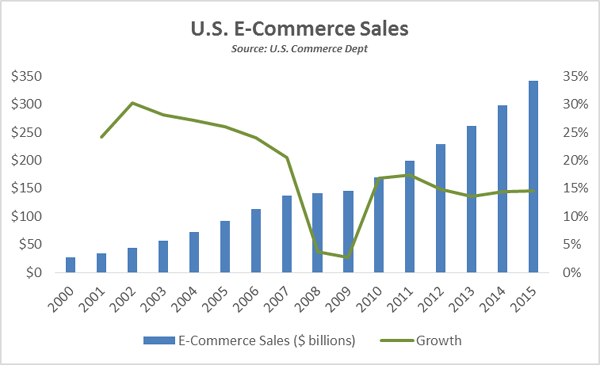

Finally Stag Industrial (STAG) owns, operates and rents 290 standalone industrial buildings, most of which are warehouses or distribution centers in hot demand thanks to the e-commerce megatrend. STAG typically acquires its properties on the secondary market where there is less competition. The firm has increased its dividend five times over the last three years. Its stock pays 5.6% today.

E-Commerce Sales Booming in America

As much as I’m intrigued by these three lesser-known REITs, my three favorite hidden gem REITs operate healthcare facilities that are in constant demand – namely skilled nursing facilities and hospitals.

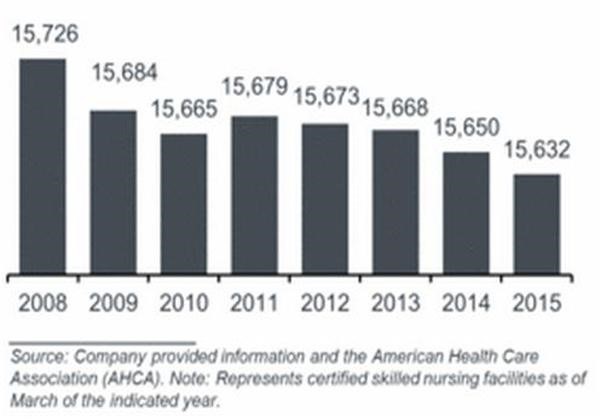

Skilled nursing is a particularly hot area. These homes provide the highest level of care an older adult can receive while still living independently. Residents generally get their own room, their own bed, and a private bathroom. Many folks are able to enjoy their remaining years here in relative comfort.

While demand is going to keep climbing (with the 65+ population set to double in the years ahead) supply is actually decreasing. We have less skilled nursing facilities today than we did in 2009!

Skilled Nursing Supply is Actually Decreasing

Rising demand and falling supply have these specialty providers well positioned to grow their dividends in the years ahead no matter what happens in the election, economy or stock market.

They are the perfect examples of hidden gems the masses are slowly starting to uncover. But both are still better bargains than the big names held by VNQ. They pay yields between 6% and 8% – up to double the ETF – and one firm is actually increasing its quarterly dividend every single quarter!

I recommend buying these undercover REITs right now, before the armchair indexers discover these recession-proof cash machines. Click here and I’ll give you the names of the three companies capitalizing on the biggest demographic shift in US history (along with stock tickers and buy prices).